Jan'23

The IUP Journal of Organizational Behavior

Archives

Corporate Social Responsibility Disclosure Practices in Indian Tea Companies

Daithun Narzari

Research Scholar, Department of Social Engineering, Rajiv Gandhi National Institute of Youth

Development, Post: Sriperumbudur, Tamil Nadu, India; and is the corresponding author.

E-mail: daithunnar@gmail.com

Sharmistha Bhattacharjee

Associate Professor, Department of Sociology, Rajiv Gandhi National Institute of Youth Development,

Post: Sriperumbudur, Tamil Nadu, India. E-mail: sharmistha.rgniyd@gmail.com

The purpose of the study is to examine the Corporate Social Responsibility Disclosure (CSRD) practices of 15 tea companies in India. It also analyzes their mode and focus of Corporate Social Responsibility (CSR) implementation. The study aims to provide evidence on how companies comply with CSRD provisions. The findings reveal that a majority of the companies, i.e., 70.66% (average from five indices), comply with the provisions of CSRD. Four of the 15 companies implement CSR directly, two through implementing agencies, and nine through both direct and implementing agencies. Schedule (i), Schedule (ii), Schedule (iv), Category B (healthcare programs), Category E (environmental sustainability), and Category C (primary education and vocational training) are the top focus areas of CSR. CSRD compliance, communication, and intervention between management, stakeholders, and government help address the problems of plantation workers. The study broadens one's understanding of CSR and CSRD practices and fills the lacuna in the literature on the tea Industry's CSR practices.

Introduction

Even after 150 years since the tea industry started in India, there continue to be debates and discussions on the poor socioeconomic and working conditions of tea plantation workers. Tea is the second most-consumed drink in the world after water. Employing roughly between 1 to 1.5 million directly and another 10 million indirectly, it is the largest private sector employer in the country. The tea industry is an important source of revenue for many states, thereby contributing to the country's economy. There has not been much improvement in the socioeconomic condition of tea plantation workers despite the existence of several laws and legislations. Human rights violations in tea industry are persisting.

The tea industry is beset by several problems. The organizational structure of the tea industry is exploitative. It is reminiscent of the British colonial system. Tea plantation workers inherently have been exploited since the inception of British colonial times, and even after 70 years of independence, the situation remains the same. The tea workers are deprived of basic human needs. The Plantations Labour Act, 1951, was formulated to improve the living conditions of the workers by providing them the basic necessities. Many empirical scholarly articles showed the management violating most of the provisions of the Act, perhaps there is no mechanism to punish the defaulter. Their problems of low wages and poor working conditions have been continuously ignored and hence their plight remains the same for generations. Despite the frequent reports on the plight of tea plantation workers, there is a lack of robust debates, discussions, and systematic research to understand the crux of the problem facing the tea industry.

In the light of the above problems of the tea industry, the paper attempts to answer how the tea companies, through CSR, can substantially overcome the problems in general and those of tea industry plantation laborers in particular. Through exercising CSR, the management of the companies has the scope to regain the trust of the people. The media discourse on the murky state of affairs in the tea industry and their questions on the tea industry's responsible behavior and ethical issues may be revamped. There has been little attention from scholars and researchers to the problems of tea plantation workers, which underscores the joint failure of the market, state, and civil society. With reference to the provisions of Section 135 of the New Companies Act, 2013, this paper aims to study the compliance practice on CSRD of tea companies in India.

Five indices in connection with CSRD have been taken, viz., availability of CSR policy on the company website, availability of annual report of the companies, disclosure of CSR in the annual report, details of CSR committee in CSR policy, and prescribed CSR format in annual report as per the Act. Under Section 135(4) of the Act, "the Board of every company referred to in Section 135(1) shall, after taking into account the recommendations made by the CSR Committee, approve the CSR policy for the company and disclose contents of such policy in its report and also place it on the company's website, if any, in such manner as may be prescribed, also ensure that the activities included in CSR policy of the company are undertaken by the company" (Chaudhary and Chaudhary, 2014). Today, corporates publish CSR information to communicate their ethical and social behavior to a wide range of stakeholders. Secondly, the researchers aim to study the mode of CSR implementation followed by the focus sectors/areas of CSR. Direct implementation of CSR helps the stakeholders participate in the decision-making of CSR implementation through discussion and dialogues, and understanding the needs of stakeholders and their priorities creates a sense of inclusiveness among the management and the stakeholders. The study will enable us to answer the questions related to tea industry's CSR practice and the initiatives undertaken by the industry. The study outlines the attempt by the tea industry in exercizing their social responsibility and the industry's compliance with CSRD provision thereof.

To accomplish the study objectives, the researchers have used secondary sources of data. The data and information are gathered from the National CSR Portal, the company's website, and the company reports available in the public domain. The study applied content analysis. The data from 15 tea companies in India have been analyzed using SPSS. The study will be useful to all the stakeholders of the companies as it portrays the company's reporting and disclosure of CSR activities. It reflects the ground reality of CSRD that may be beneficial for companies to decide CSRD patterns efficiently. It can be an informative piece to the management, stakeholders, and policymakers. More importantly, this study will identify the industry's priority sectors/areas, the areas that are still untouched, and the untapped areas of CSR implementation. The study will fill the lacuna in the literature on the tea industry's CSR practice.

In the current context, it will be wise for the tea companies to comply will all the CSRD provisions, ensuring transparency through reporting and communicating CSR, aiming to build a trustworthy relationship with its stakeholders. The study is limited to 15 tea companies under the purview of mandatory CSR.

Literature Review

Section 135 of the New Companies Act, 2013, has made it mandatory for companies to participate in CSR activities. Corporate participation in CSR can help address socioeconomic and environmental concerns. According to the Indian Institute of Corporate Affairs, there are 6000-7000 companies in India under the purview of CSR as per the New Provision of the Act. Spending 2% of their profit on CSR activities will lead to an annual CSR spending of 150,000-200,000 mn, which will ensure a better standard of life for people (Sharma, 2013). As of January 31, 2022, based on the data available on the National CSR portal, there are 18,292 CSR contributing companies in India, spending a total of 1,096,920 mn from FY 2014-15 to 2020-21 (National CSR Portal).

Tea Industry

Since the discovery of tea by Emperor Shen Nong in 2737 BC, it has been one of the cheapest and most widely consumed beverages (Hazarika, 2011). The tea industry has largely benefitted the economy of tea-producing countries such as India, China, Kenya, and Sri Lanka. It plays a vital role in a nation's economy through foreign exchange earnings (Gunathilaka and Tularam, 2016). India is the second-largest tea-producing country with a share of 23% after China. 98% of tea is produced in four major tea growing states, viz., Assam, West Bengal, Tamil Nadu, and Kerala. Assam alone accounts for 51% of tea production. Tea is important revenue for various states/UTs; it is a major contributor to the foreign exchange reserves of the country. A large chunk of the remote population from different corners of the country are engaged in gainful employment directly and indirectly.

Problems of the Tea Industry

The laborers in tea plantations are portrayed in popular media as joyful people smiling, singing and dancing to the music of nature on rolling green hills. This is far from reality on the ground (Sarma, 2019). The tea laborers and employees lead miserable lives. The challenge is to meet their basic necessities and improving the economic condition of communities dependent on tea plantation. There is an abundant need to study the country's failure to address their livelihood concerns (Tirkey and Nepal, 2012). A majority of the tea workers employed in plantations called tea estates are wage laborers. 50% of workers are estimated to be women. They are the third and fourth generation of migrants initially brought by the British from the central part of India; a majority of them are from lower castes and tribals belonging to the lowest strata of the society (Vijayabaskar and Viswanathan, 2019). Despite the fact that the tea sector employs more women, the female employees remain neglected. Gender and class intersectionality exists on tea estates.

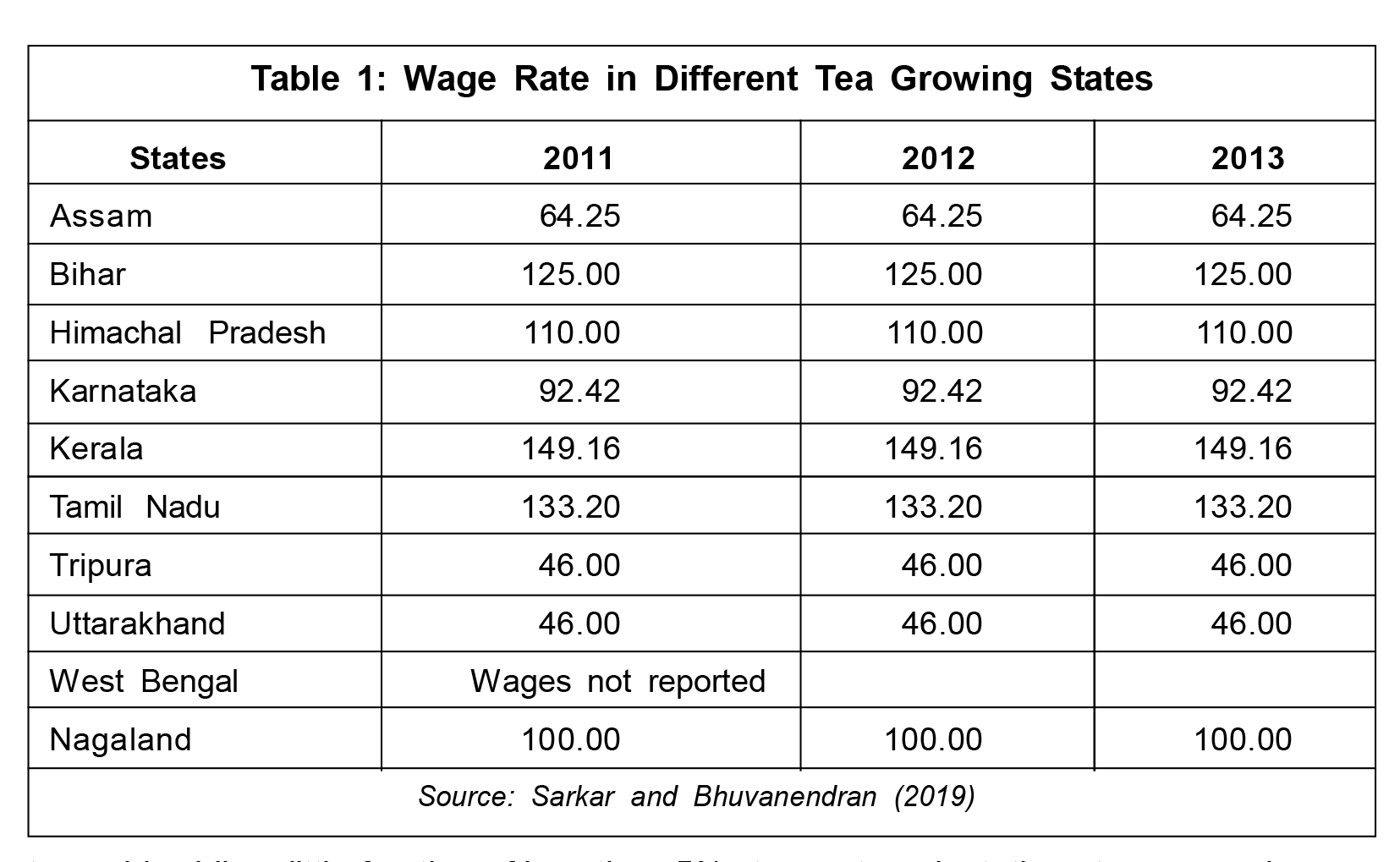

Female workers are subjected to verbal and physical violence both at work and at home. Plantation employment is gendered, and women employees continue to work in hazardous circumstances (Duara and Mallick, 2019). They have traditionally been confined to the bottom strata and seen as the most numerous and cheapest labor force rather than a source of specialized labor (Gurung and Mukherjee, 2018). The laborers on tea plantations were found to have nutritional abnormalities. The 15-35 age group of employees was most impacted by anemia, and the female workers in this group were most afflicted throughout their reproductive years (Ganesan and Saravanabavan, 2018). India's tea industry is beset by the issue of low pay, which led to unfavorable living and working circumstances. Northeast region tea plantation workers and their families are experiencing starvation-related mortality. Tea workers have the lowest pay among plantation employees, particularly in the northeast region. Workers are now living in complete poverty as a result of the unjust pay structure, management's lack of interest, the state government's failure to enforce regulations, and the Union government's ineffective surveillance. There is no standard wage structure for plantation crops or tea across states. Except for Nagaland, where the minimum wages given for the year 2013 are higher than all the states taken into consideration, there is clear evidence of very low minimum wages for the North Eastern states in comparison to Southern states in the case of tea (Sarkar and Bhuvanendran, 2019) (Table 1).

The plantation workers received a wage of about $1-1.5 a day, which is among the lowest in the world and even lower than the wages received in Sri Lanka and Kenya. In an industry where companies are earning billions of dollars of profit, their employees and laborers face the worst form of exploitation. They have a very low literacy rate, and due to the non-availability of other livelihood options, their children are left with no other option but to completely depend on tea plantations under abysmal conditions (Vijayabaskar and Viswanathan, 2019). Tea companies and supermarkets take a substantial cut up to 95% in certain circumstances for every kilogram of packaged Assam tea sold, while a little fraction of less than 5% stay on tea plantations to pay employees. These disparities in how the portion of the final consumer price of tea is divided lead to poverty and misery for the women and men working on Assam tea plantations, while also generating a sustainability issue in parts of India's tea sector. Tea plantation workers in India's Assam area are systematically denied their right to a fair wage and acceptable working and living circumstances (Banerji and Willoughby, 2019).

Other than the historical disadvantages of tea workers due to exploitative management- labor relations, the study highlighted various incidents of tussles between the management and the labor. They have reported 14 violent cases between 2003 and 2019 which compelled the workers to take extreme steps. Most of the cases are due to denial of basic necessities by the management, payment of inadequate wage, undesirable management attitude, and molestation. The existing wage paid to the workers is not sufficient to live a decent life, resulting in low standard of living. They should receive a 'living wage' supplemented with proper non-cash benefits and welfare amenities leading to decent living conditions.

According to Saha et al. (2019), 'about 48% of workers receive in-hand income ranging from 3,500 to 4,000 while another 39% receive in the range of 4,000-4,500 per month'. Dutta and Basu (2017) reported the adverse living conditions of tea garden workers. The tea communities live a simple and honest life that needs basic requirements such as food, shelter and medical support. Women comprise a large proportion of tea plantation workers in India. They are mostly illiterate and are restrained from education amid poverty (Bosumatari and Goyari, 2013). The adoption of labor legislation, particularly PLA and India's independence gave the sector's labor relations and welfare a new dimension. It was understood that improving labor welfare might boost productivity and foster favorable interactions between companies and employees. From this perspective, it is important to remember that India's PLA dates back to more than 50 years. It explicitly outlines the welfare measures that plantation owners must offer to their workers, but there is still no proof that these laws are being implemented in an efficient manner (Sumitha, 2012). The Plantation Labour Act, 1951 constitutes a comprehensive provision for labor welfare in India. The Act includes several provisions for the upliftment of plantation workers. Despite all the legislative provisions, the tea plantation workers remain marginalized and vulnerable. Issues such as their poor working conditions and underpayment remain ignored and unaddressed (Gupta et al., 2017). According to the Plantation Labour Act, 1951, every tea estate (land used for growing tea with an area of 25 ha or more, where 225 persons or more are employed) is mandated to provide basic necessities for the employees and laborers of their estate. These include housing facilities, residential facilities, healthcare facilities, maternal benefits, canteen, rations, drinking water, education facility, etc. (Bora, 2015). In the year 2013, with the help of three local non-governmental organizations DBSS, PAJHRA, and PAD, the workers filed a report on violation of wage and labor laws, poor hygiene, restrictions on freedom of association, hazardous conditions for pesticide sprayers, and concerns with the share program. The report was filed with World Bank's Compliance Advisor Ombudsman (CAO). After three years of investigation, CAO released its final report confirming most of workers' complaints (Thacker, 2019). In the present context of changing socioeconomic and political scenarios, the PLA needs thorough revision. The tea estates still function under a master-slave system of colonial times (Khawas, 2011). Only through strict policy implementation and government intervention, the scenario can be changed. To address the social security issues and ensure the positive impact of labor acts, more research needs to be conducted in the area (Rafeeque and Sumathy, 2021). The tea workers' crisis can only be resolved if trade unions and the government recognize their duties; otherwise, the chances for considerable changes in economic and social wellbeing may be gloomy, if not impossible (Gurung and Mukherjee, 2018).

Tea Industry's Social Responsibility

Kadavil (2005) stressed the need for strategic CSR, taking into account the stakeholders significant for the business. Based on a study of three tea estates in the state of Assam, Goowalla (2014) concluded that the tea industry, through CSR, provides various facilities, benefitting plantation workers; however, the beneficiaries are unaware of the facilities provided. Tea plantation management should focus on sustainable development, business ethics, human rights, rights and labor regulations, human resource management, and corporate governance procedures, and embrace best practices in these areas. To avoid environmental disruptions, businesses should closely adhere to environmental laws, rules, and regulations. The corporation has an ethical obligation to contribute to the creation of a sustainable environment by preserving ecological balance (Wijerathna and Gajanayaka, 2014). The facilities provided under the PLA, 1951 to employees and laborers of the tea estate are not considered CSR activities of the tea companies (Bora, 2015).

Corporate Social Responsibility Disclosure

Companies disclose CSR information in different ways: through annual reports, corporate websites, interim and quarterly reports, articles published on CSR activities, advertisements, booklets, environment reports, press releases, employee reports, etc. (Sufian, 2012). According to Baskin and Gordon (2005), one-third of the emerging market companies either have a separate section on their website for CSR or produce sustainability reports on CSR in their annual reports. There has been an increasing awareness of public, academic, media, and regulatory bodies regarding the importance of CSR practice of business organizations and their reporting. It has resulted in increasing disclosure of CSR information to satisfy their wide range of stakeholders and to establish a positive image in the market and society (Ehsan et al., 2018). Saha (n.d.) observed that the companies chosen for their study had significantly increased their CSR disclosure practices as a result of widespread knowledge of the Companies Act, 2013. Today, the Internet is one of the main tools for the disclosure of CSR information, which allows companies to publish more information at minimum cost and on a faster mode than before. This has enabled the companies to communicate ethically and responsibly through their websites to their diverse stakeholders (Soares et al., 2008). It entails measuring and reporting internal and external information on the social impact of an activity (Mahadevappa and Rechanna, 2012). According to Bayoud and Kavanagh (2012), financial managers reveal that CSRD is important for the performance of the company. Social responsibility disclosure is an indicator of improved CSR practice and it affects the company's reputation. Platonova et al. (2016) opined that in the case of GCC Islamic banking, the bank's profitability had a positive relationship with the higher level of CSR disclosure. Hassan (2010) pointed out that it is evident that despite CSRD having no impact on corporate market value, CSRD significantly influences corporate social reputation. Although the need and benefit of active and transparent CSR communication is widely acknowledged, the value of such open communication has not been fully recognized by the companies (Chaudhri and Jian, 2007). Dyduch and Krasodomska (2017) found that a company's social and environmental performance has an impact on the general performance of the company. On the other hand, Worokinasih and Zain (2020) opined that CSRD does not significantly affect the value of the firm and added that CSRD can be considered by the investor before their capital investment; however, their findings indicate that the investors do not have a positive response to CSRD.

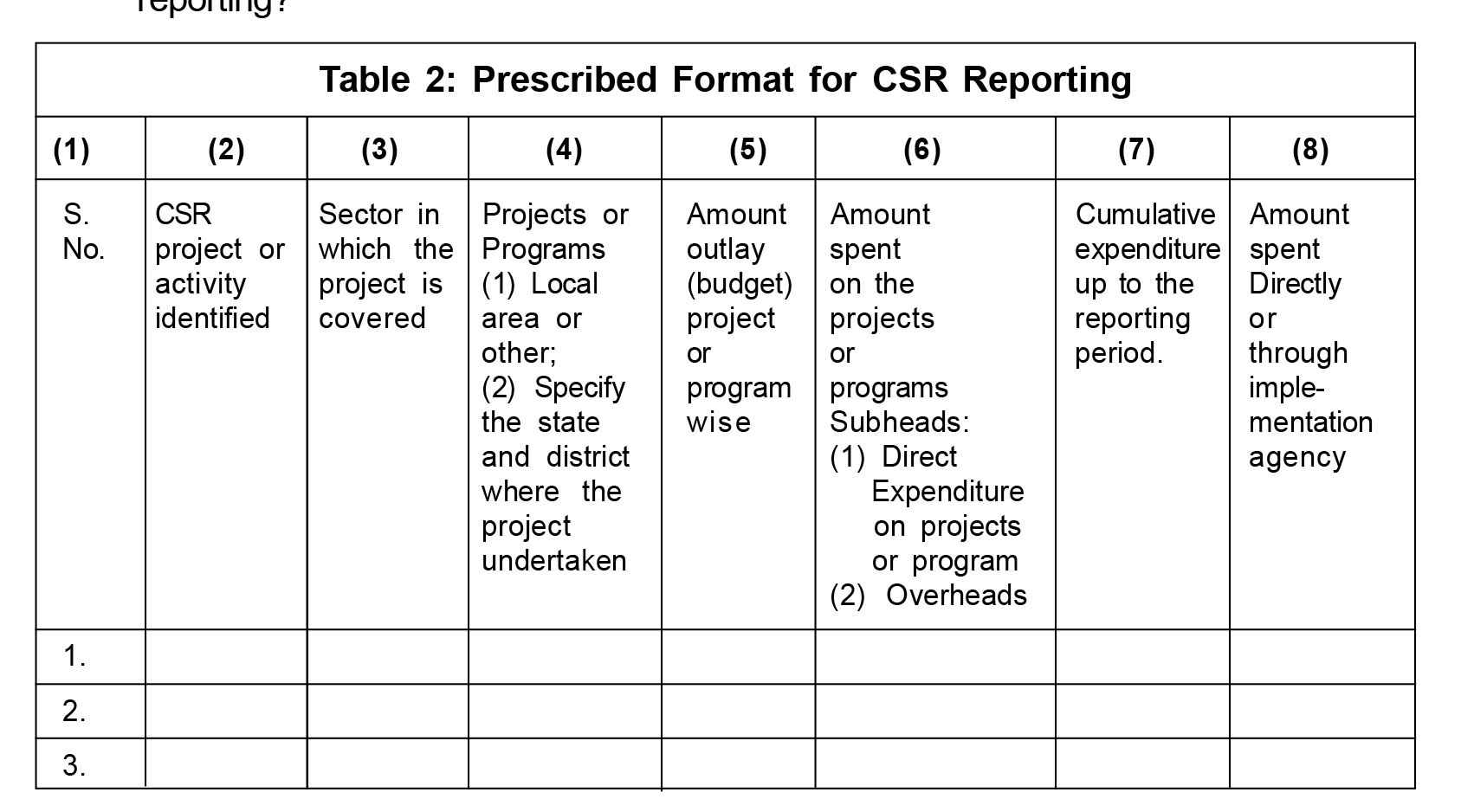

Not only India, countries like Malaysia and France also mandate CSR disclosure in companies' annual reports (Dyduch and Krasodomska, 2017). CSR reporting among Indian firms now has new, obligatory aspects, thanks to the Company Bill, 2013. In order to generate the next wave of innovation and product development in the global economy, the corporate sector in India must thus change the way it approaches business (Bhatia and Chander, 2014). As per Section 135(4), the Board of Directors of the company shall, after taking into account the recommendations of the CSR Committee, approve the CSR Policy for the company and disclose the contents of such policy in its report, and the same shall be displayed on the company's website. The prescribed CSR format needs to be maintained as per the Act when reporting CSR in the company's annual report (Ministry of Corporate Affairs - Government of India, 2014) (Table 2).

A company under the purview of CSR as referred to in Section 135(1) has to mandatorily comply with the provisions of the Act every year. However, Rule 3(2) of the CSR rule 2014 provides that if a company ceases to meet any criteria for three consecutive financial years, it is not required to follow the provision until it again fulfills the applicable criteria (Jain, 2015). Schedule vii of the Act includes the following sectors/areas of CSR that can be undertaken:

Schedule (i) eradicating hunger, poverty, and malnutrition, promoting preventive health care and sanitation, and making available safe drinking water.

Schedule (ii) promoting education, including special education and employment enhancing vocation skills, especially among children, women, elderly, and the differently-abled, and livelihood enhancement projects.

Schedule (iii) promoting gender equality, empowering women, setting up homes and hostels for women and orphans; setting up old age homes, daycare centers, and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups.

Schedule (iv) ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agroforestry, conservation of natural resources, and maintaining the quality of soil, air, and water.

Schedule (v) protection of national heritage, art, and culture including restoration of buildings and sites of historical importance and works of art; setting up public libraries; promotion and development of traditional handicrafts.

Schedule (vi) measures for the benefit of armed forces veterans, war widows, and their dependents.

Schedule (vii) training to promote rural sports, nationally recognized sports, paralympic sports, and Olympic sports.

Schedule (viii) contribution to the Prime Minister's National Relief Fund or any other fund set up by the Central government for socioeconomic development and relief and welfare of the Scheduled Castes, the Scheduled Tribes, other backward classes, minorities, and women.

Schedule (ix) contributions or funds provided to technology incubators located within academic institutions which are approved by the Central government.

Schedule (x) rural development projects (Ministry of Corporate Affairs, 2014).

Based on the above discussion, we framed the following research questions:

1. Do the companies report their CSR activities and CSR policies on their websites/annual reports?

2. Do the companies disclose the details of the CSR committee in their CSR policy?

3. Do the companies follow the prescribed format, as per the Act, for CSR reporting?

4. What are the modes of CSR implementation?

5. Which are the focus sectors/areas of CSR implementation?

Objectives

- To study the CSR disclosure practice as per Section 135 of the New Companies Act, 2013;

- To elucidate the mode of CSR implementation; and

- To analyze the focus sectors/areas of CSR implementation.

Data and Methodology

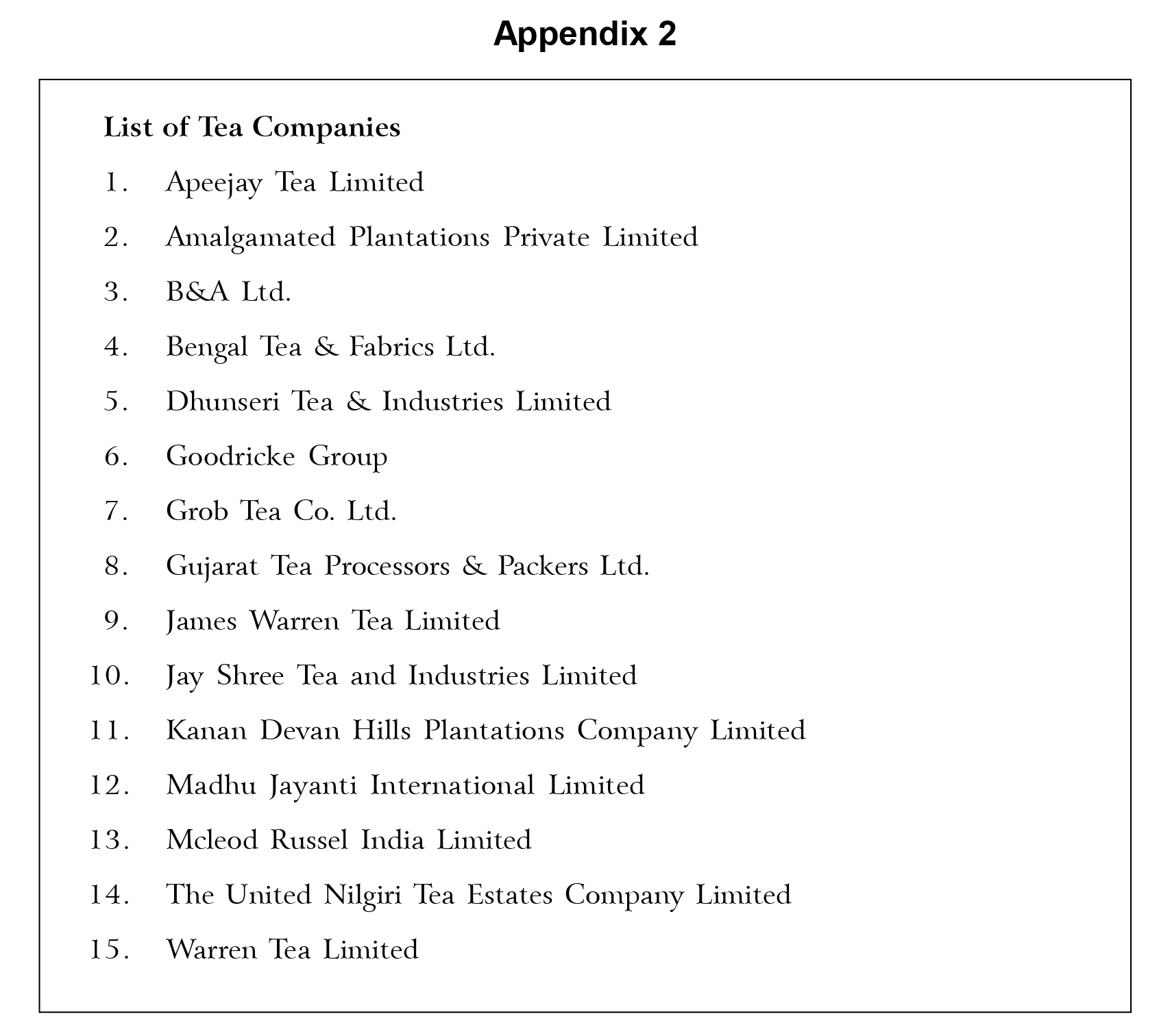

The sample of the study are the tea companies in India under the purview of mandatory CSR. Fifteen companies (see Appendix 2) were selected using a purposive sampling method with the criteria (i) companies involved in tea plantation activities; and (ii) companies in the bracket of mandatory CSR from the financial year 2014-2015 to 2020-2021.

The study is based on secondary data, i.e., academic journals, articles, thesis, books, reports, company website, newspapers, and magazines. To obtain empirical findings, National CSR Portal, annual reports, and the company's website that are available in the public domain till January 31, 2022, have been used. The annual report is the most commonly used document in the analysis of corporate social activities. The frequency of using annual reports is justified by their regularity, credibility, accessibility, and useful pieces of information to stakeholders reporting (Dagiliene, 2010).

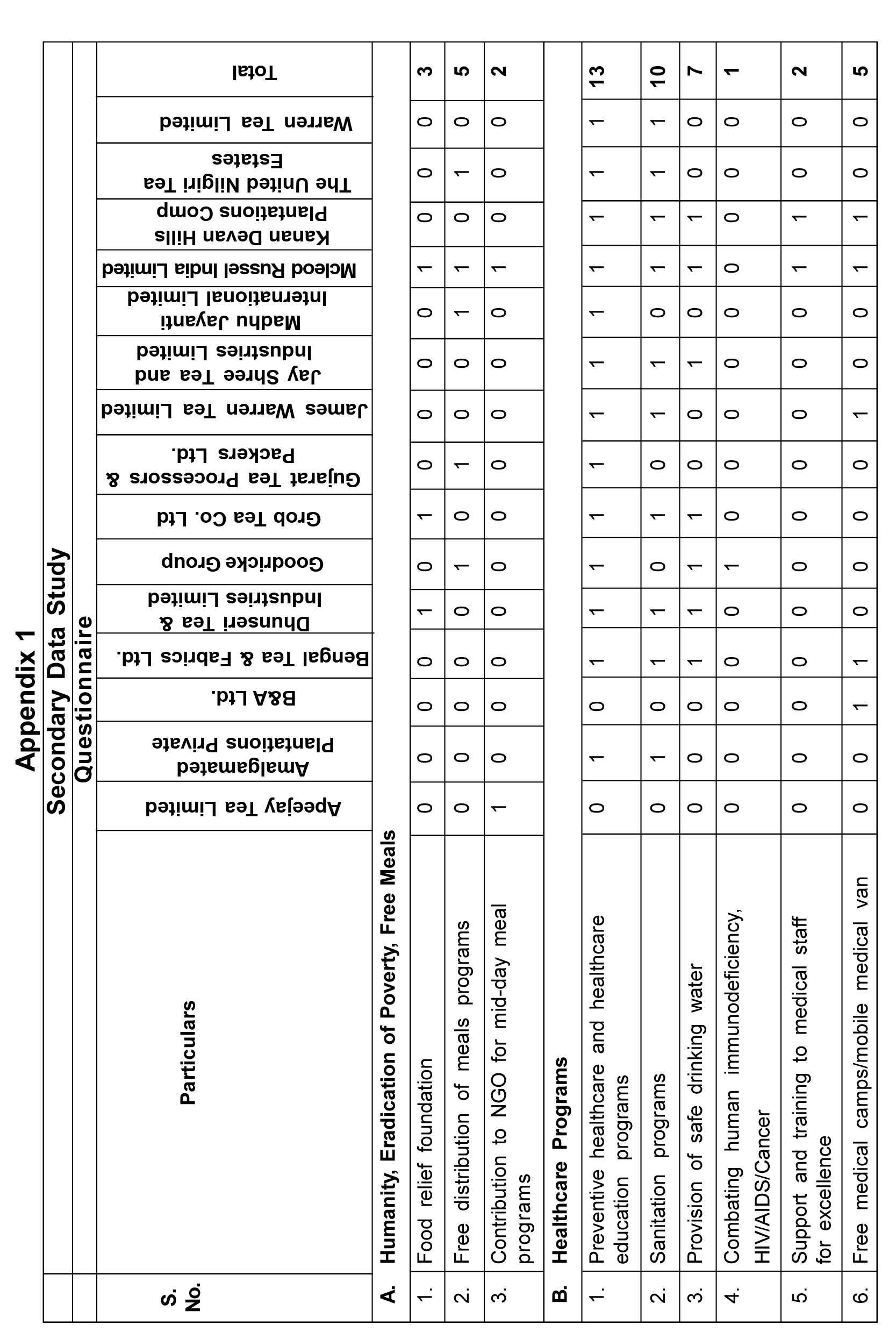

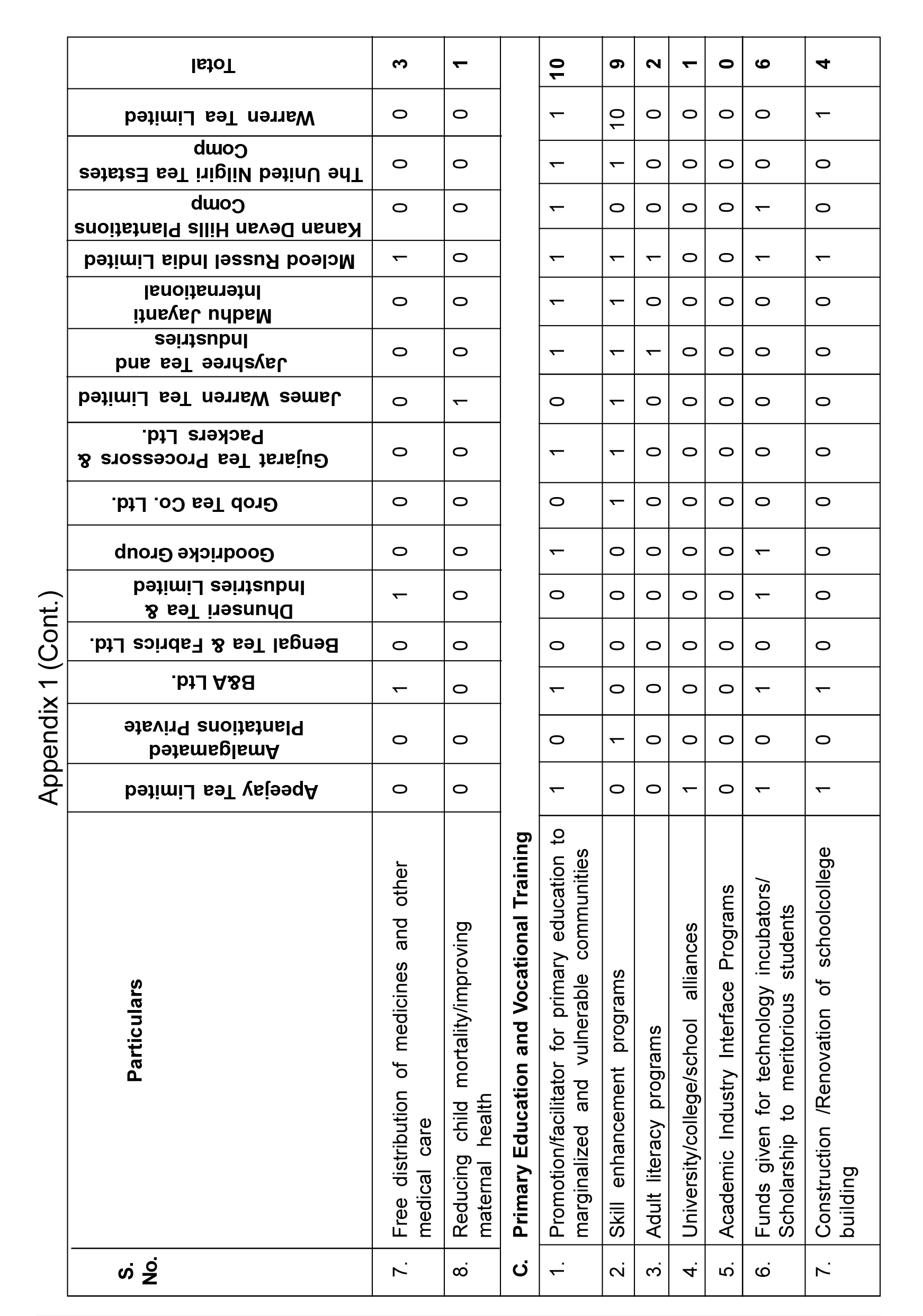

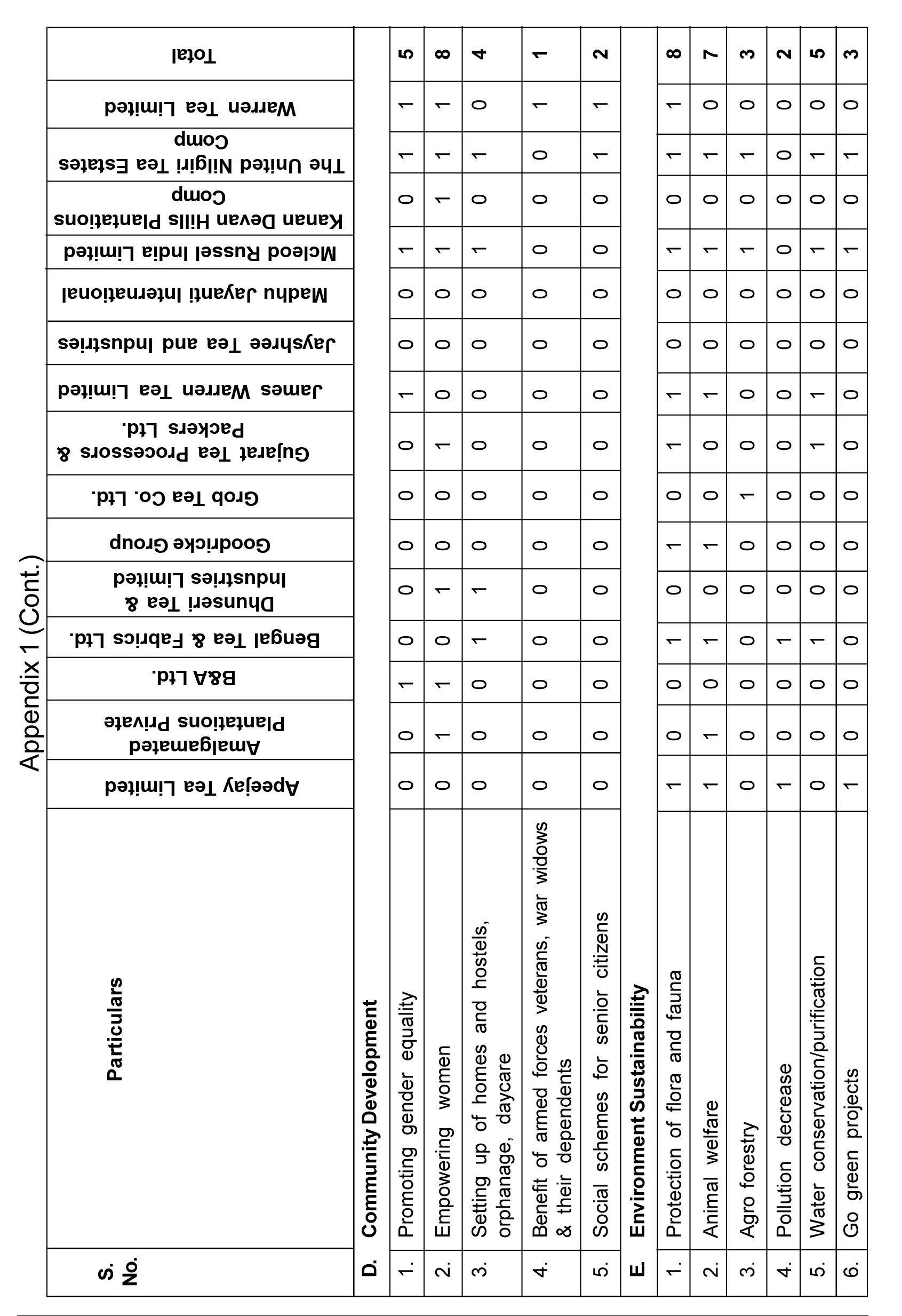

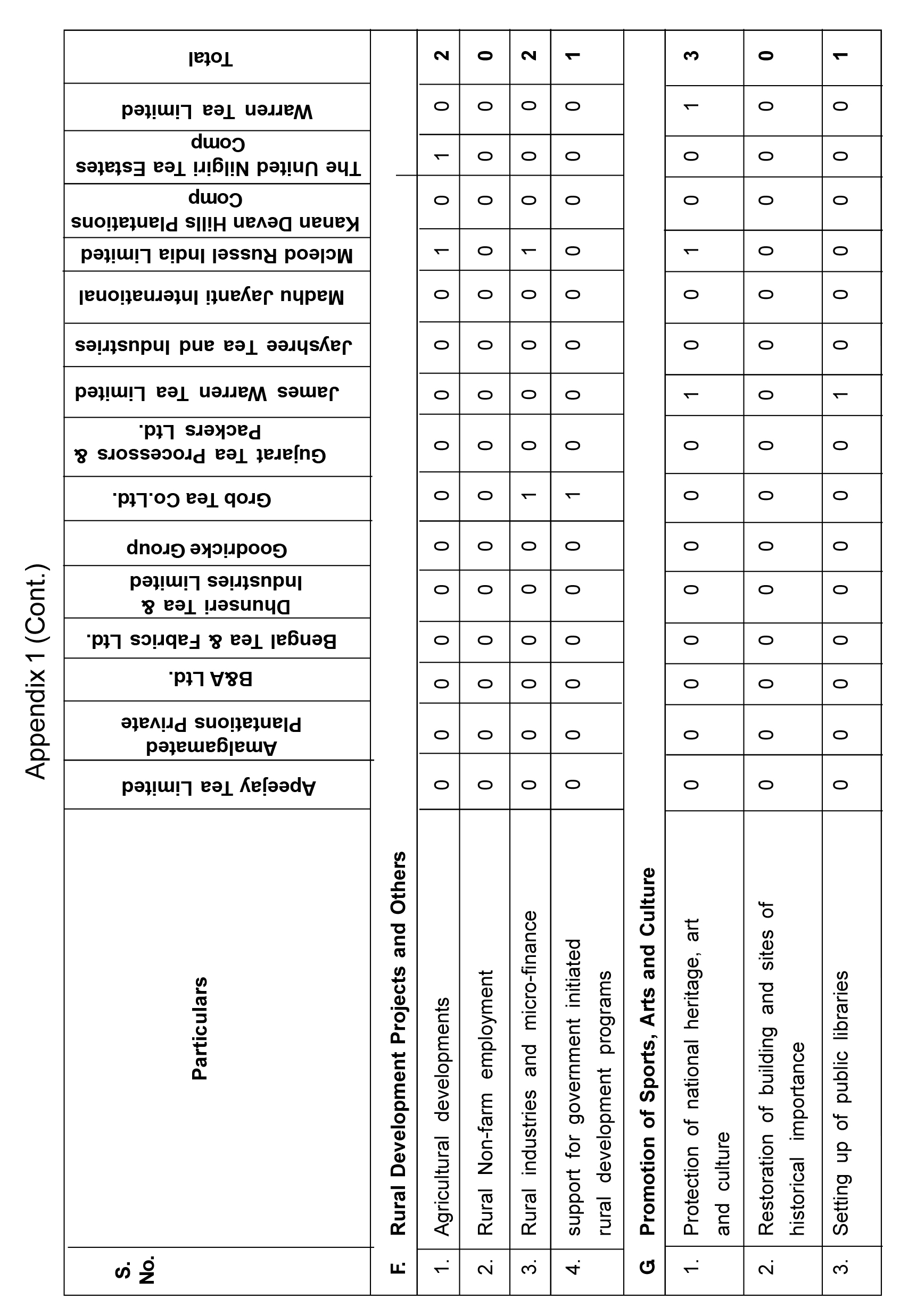

A quantitative approach of descriptive design using secondary data is deployed for the study (Appendix 1). The study applied content analysis. Content analysis is one of the most important techniques in social science research. The most apparent source of data for content analysis is text, namely, spoken dialogue, written documents, and visual representations, to which interpretations are typically ascribed. The methodical handling of content analysis data is primarily responsible for the capacity to support inferences that go beyond the unassisted reading of the text (Krippendorff,1989). It uses a series of processes to draw valid inferences from the text. It categorizes textual data, reducing it to more relevant, understandable chunks of information employing a variety of ways to build categories and variables. Certain investigators manually count a few keywords or phrases. Others have built a series of content categories around a particular theme. Another method of content analysis is the design and use of broad dictionaries (Henkel,1976).

The method is also quite adaptable in that it may be either theoretically or empirically driven. Written text is by far the most often used data source for content analysis (Stemler, 2015). The technique's emphasis on content analysis of data coding and categorization is what makes it exceptionally rich and valuable (Stemler, 2000).

Based on the criteria, a score of 1 or 0 has been given for coding. If the "CSR disclosure indices" (Table 3) are available, a score of 1 is given; otherwise, a score of 0 is given. If a company implements CSR directly, it obtains a score of 1; otherwise, it obtains a score of 0, and so on for indirectly implemented CSR and both. For "Sector/Area wise CSR implementation" (Table 5), a company obtains a score of 1 if CSR activities are carried out in a specific sector or area listed in Schedule VII, and a score of 0 if no such activities are carried out. Additionally, we use the CSR disclosure index developed by Haldar (2015). The disclosure index is developed using the elements specified in the modified Schedule vii of the 2013 Firms Act, released on February 27, 2014. It is used to assess the CSR disclosure practices of sample companies. Based on the disclosure index, a rating sheet was created to assess the sample company's social responsibility activities. A company scores 1 if it discloses a piece of information from the index, and score 0 if it does not, and thereafter category-wise score and the item-wise score are calculated. The frequency and percentage are obtained from descriptive statistics using the Statistical Package for the Social Sciences (SPSS). The derived frequency and percentage from the analysis are displayed in

Tables 3 to 6.

Findings

The findings on CSRD with respect to five indices of tea companies in India are discussed below.

Section 135(4) of the New Companies Act, 2013, in India mandates companies that fall under the ambit of CSR defined under the Act to follow the five indices that we have chosen for the study.

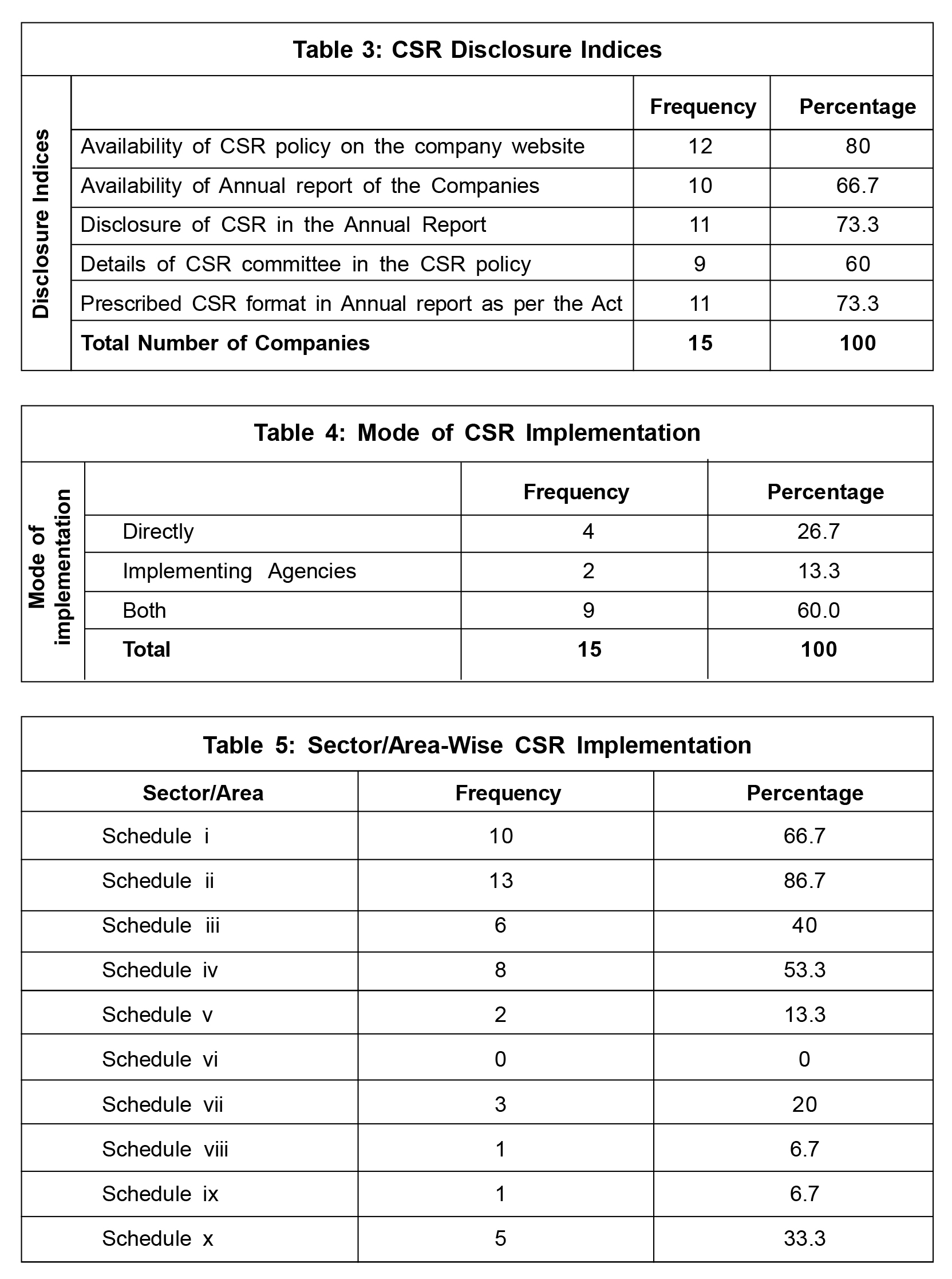

Availability of CSR Policy on the Company Website: Table 3 shows 12 companies out of 15, i.e., 80% have a CSR policy on their company's website. Companies may have a separate tab or section for CSR, but may not include the detailed CSR policy of the company.

Availability of Annual Report of the Companies: For 10 companies, i.e., 66.7% of the companies, annual reports are available on their company's website. The annual reports of five companies are not available on their website.

Disclosure of CSR in the Annual Report: 11 companies, i.e., 73.3%, disclose CSR activities in their annual report. Out of 15 companies, four companies, i.e., 26.7% of the companies, do not disclose the CSR activities in their annual report. A few companies are active on their website, highlighting CSR activities, but are silent in their annual report.

Details of CSR Committee in the CSR Policy: Nine companies, i.e., 60%, provide the details of the CSR committee in the CSR policy available on their website. Detailed disclosure of the composition of the CSR Committee is required as per the Act.

Prescribed CSR Format in Annual Report as per the Act: Out of 15 companies, 11 companies follow the prescribed format in the annual report as provided in the Act.

Table 4 shows the findings on the mode of CSR implementation of 15 tea companies in India.

Direct: Only four companies out of 15, i.e., 26.7%, implement CSR directly.

Through Implementing Agencies: Two companies, i.e., 13.3%, implement through agencies.

Both: Nine companies, i.e., 60% of the companies, implement through direct and through implementing agencies.

The findings of the study on the 'mode of CSR implementation' are in line with the KPMG CSR reporting survey 2015. Their survey reveals that most of the companies, i.e., 85.90 of companies, implement CSR through direct and through implementing agencies. According to Datta and Karande (2017), direct implementation of CSR involves more transaction costs when compared to implementation through specialized agencies. Implementing through specialized agencies has an advantage for the companies that achieve a certain scale of economies, nevertheless, the effectiveness of these implementing agencies should be closely scrutinized for appropriate benefits from CSR activities (Jarwal and Kahal, 2021). The companies implement CSR directly through the CSR division, Human Resource Department, local management of manufacturing unit in CSR activities, through their own foundation, through Registered Trust, Registered Society, Company established under Section 8 of the Companies Act, 2013 by the company (Pradhan and Ranjan, 2010).

Table 5 shows the focus areas/sectors of CSR implementation of tea companies in India. The findings of focus sectors/areas are highlighted from top priorities to bottom.

Schedule (ii) 13 companies out of 15, i.e., 86.7% implement CSR in this sector/area which is the highest. This schedule broadly covers education, vocational skill, and livelihood enhancement programs.

Schedule (i) 10 companies out of 15, i.e., 66.7% perform activities related to Schedule (i), that broadly cover health, poverty, and sanitation.

Schedule (iv) Eight out of 15 companies, i.e., 53.3% of the companies perform activities covering schedule iv of the Act. The schedule broadly covers activities related to environment and animal welfare.

Schedule (iii) Six companies, i.e., 40% of the companies carry activities related to this schedule that broadly covers activities related to empowering women to promote gender equality, facilities towards old age, and reducing inequalities.

Schedule (x) Five companies out of 15, i.e., 33.3% implement CSR on rural development projects.

Schedule (vii) Three companies, i.e., 20% of the companies conduct different programs for promoting sports.

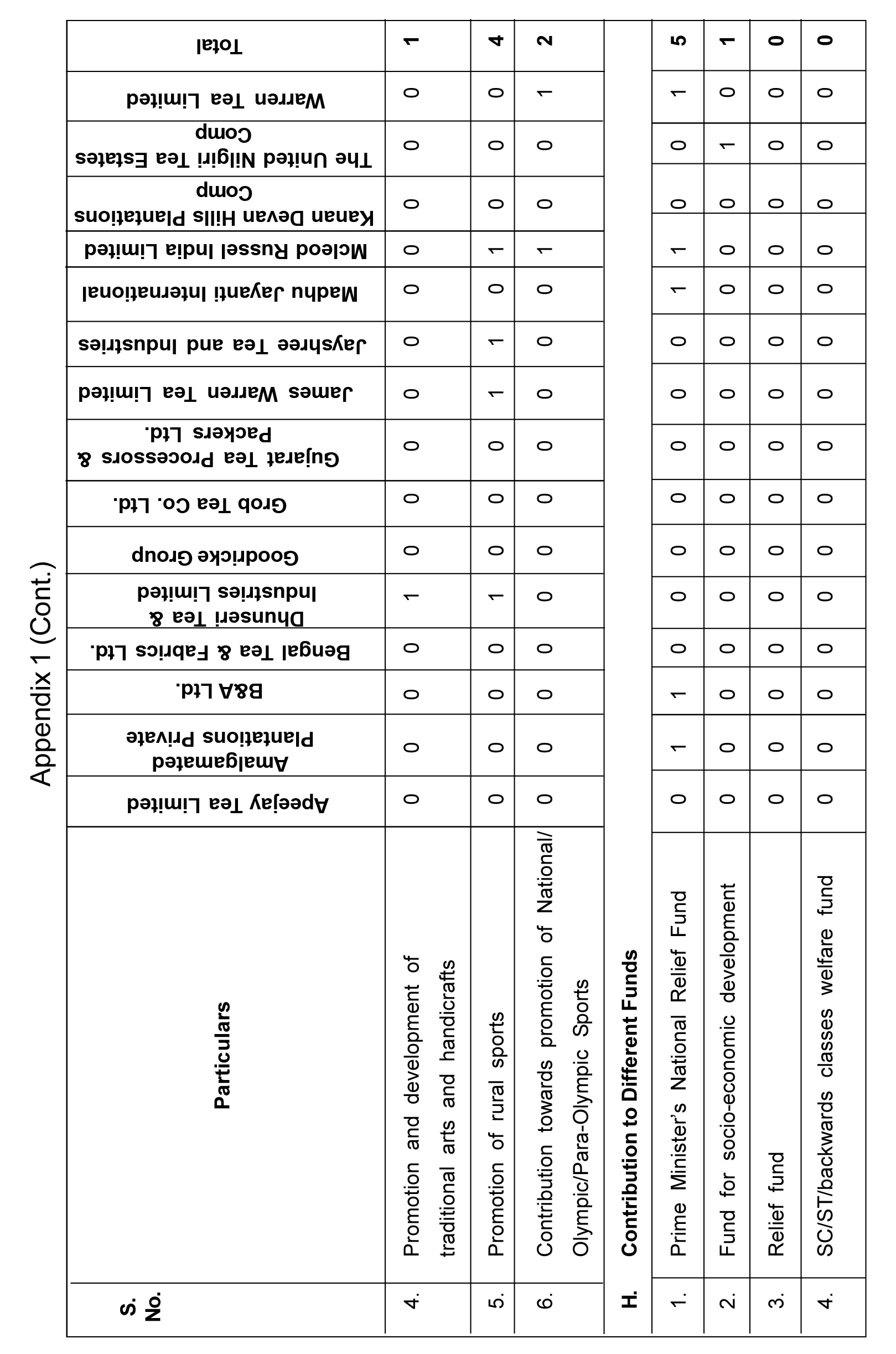

Schedule (v) Two companies out of 15, i.e., 13.3% perform CSR activities covered under this sector/area that broadly covers arts and culture, national heritage, and promotion and development of tradition and handicrafts.

Schedule (viii) includes the sector/area dealing with a natural disaster. Only one company out of 15 companies is active in solving those common problems caused by natural disasters in one of the other regions that the country faces today.

Schedule (ix) Only one company out of 15 companies contribute to promoting entrepreneurship through contributing funds towards technology incubators which is an important sector/area for an economy and nation-building.

Schedule (vi) Not a single company has undertaken activities benefitting the families of armed forces veterans who sacrificed their lives for the nation.

The findings of the study with regard to focus sectors/areas of CSR implementation are consistent with the number of studies. As per the Crisil Report (2019), the highest CSR spending head is education and skill development, followed by healthcare and sanitation. Dhaneshwar and Pandey (2015) and Das and Ray (2020) identified health and education as the top areas of attention in CSR. Education is the area that is most taken care of, followed by health (Bala, 2015). As pointed out by Ranjan and Tiwary (2018), health, education, and environment protection are the thrust areas of CSR. Education remains the top priority, followed by environment and health (Desai et al., 2018). Singh and Agarwal (2013) mentioned that community welfare is the most favored area, followed by education and health.

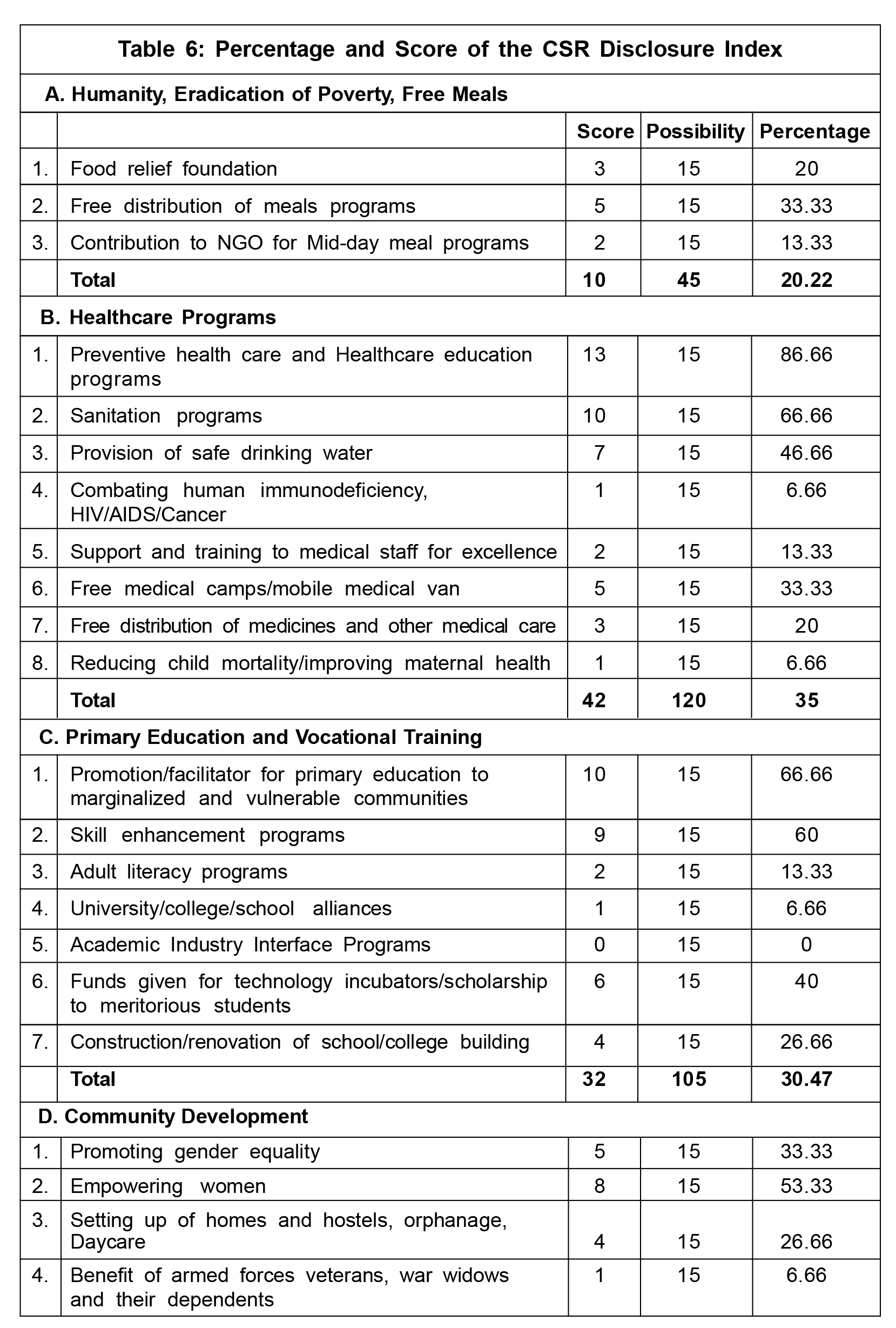

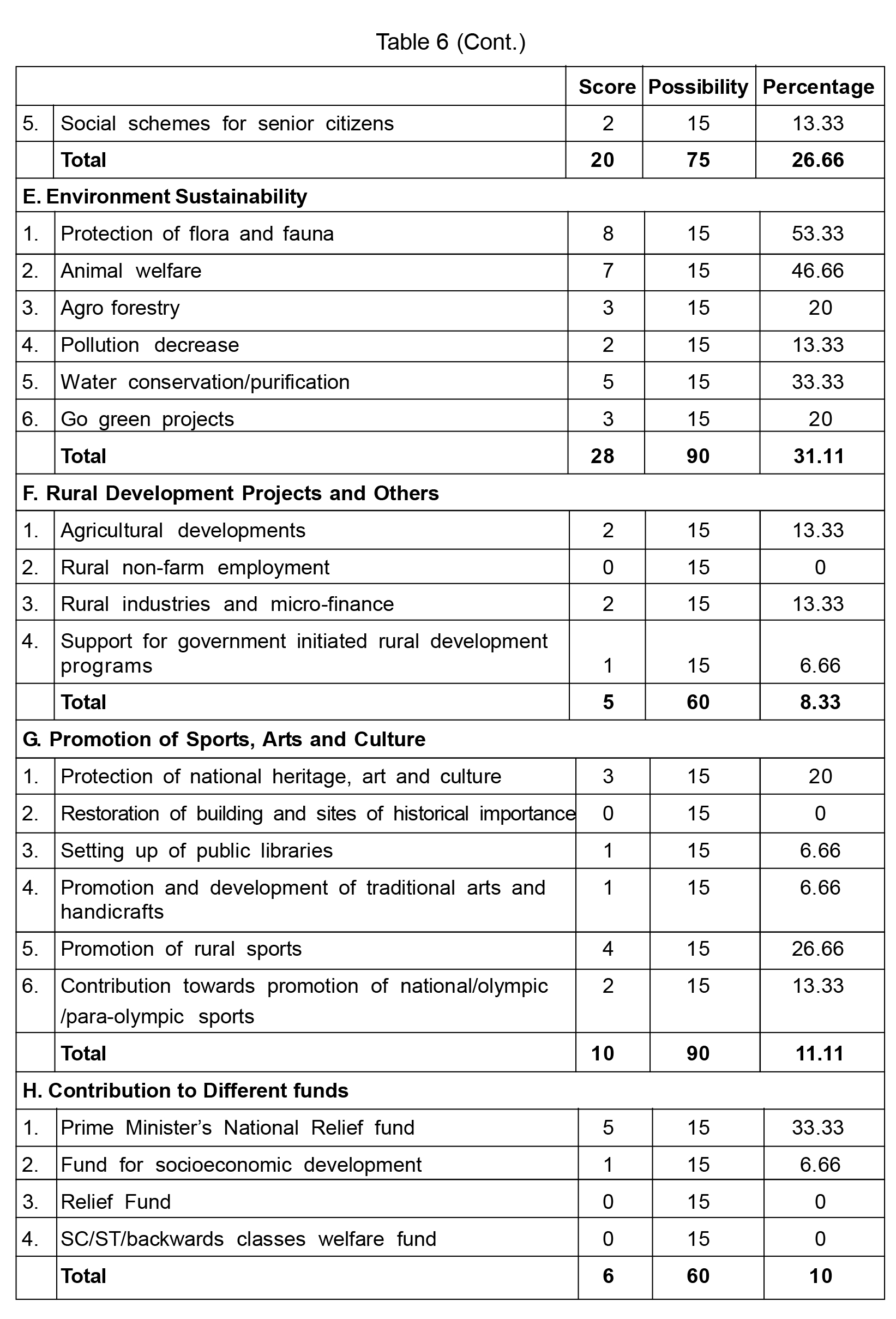

Table 6 displays the CSR disclosure index as well as individual items from each of the eight categories: A, B, C, D, E, F, G, and H. Given that there are 15 sample companies, each item in the category has a possibility of scoring fifteen. Adding all the items for each category, category A has a possibility to score a total of 45, B = 120, C = 105, D = 75, E and G = 90, and F and H = 60. For CSR initiatives of tea companies, category B-Healthcare programs, receives the highest percentage (35%), followed by category

E-Environmental sustainability (31.11%) and C-Primary Education and Vocational Training (30.47%). Considerable focus should be given to the categories D-Community Development (26.66%), and A-Humanity, Eradication of Poverty, Free Meals (20.22%). The least focus areas are G-Promotion of Sports, Arts, and Culture (11.11%),

H-Contribution to Different Funds (10%), and F-Rural Development Projects and Others (8.33%). Looking at the individual items, we found that a majority of the tea companies' CSR activities are undertaken on preventive healthcare and healthcare education programs (86.66%), followed by sanitation programs and promotion/facilitator for primary education to marginalized and vulnerable communities (66.6%). A meager less than 10% (6.66%) of activities have been dedicated to combating human immunodeficiency, HIV/AIDS/cancer, reducing child mortality/improving maternal health, University/College/School alliances, benefit of armed forces veterans, war widows and their dependants, support for government initiated rural development programs, setting up of public libraries, promotion, and development of traditional arts and handicrafts and fund for socioeconomic development. Academic Industry Interface Programs, social schemes for senior citizens, rural non-farm employment, restoration of building and sites of historical importance, relief fund and SC/ST/backwards classes welfare have not been the focus of CSR activities of any of the tea companies.

Discussion

The present study aims to contribute to the literature on CSR in tea companies by increasing the understanding of CSR practices and CSRD compliance. The objective of the paper was to examine the disclosure of CSR as per the Act, to elucidate the mode of CSR implementation, and analyze the focus sectors/areas and the CSR disclosure index. The study provided findings on tea companies' CSR disclosure based on five indices. According to Chen et al. (2018), the political/social factors of the firm largely drive CSR spending rather than economic considerations. CSR disclosure creates a positive image for society at the cost of shareholders by changing the firm's behavior. Reporting is embedded in a company's strategy and is instrumental; it is used as a tool to foster stakeholders' trust for survival and growth. However, the decision to meet the stakeholders' expectations on adopting CSR and CSR reporting is complex for the organization yet deemed necessary. Profound social reporting can harness better relationships with the stakeholders (Islam et al., 2018). The New Companies Act, 2013 has clear instructions on CSRD to the companies under the purview of CSR, yet a number of companies do not comply with the rule as per the Act. This shows a lack of seriousness on the part of CSR implementation, disclosure, transparency, and accountability. It is high time companies deploy a strategic CSR showing the transparency of their social activities which offer social as well as economic benefits along with meeting the societal expectation.

Today, in response to the increasing demand of stakeholders and legitimate business operations, CSR information is the major part of a company's corporate disclosure. It is a reflection of the company's performance (Michaels and Gurng, 2018). 60% of companies implement both directly and through implementing agencies. Only 26.7% of companies implement it directly. The benefits of direct CSR implementation need to be addressed and government intervention is required to make a visible difference. Effective CSR implementation can be done through direct involvement of the companies while today most of the companies implement through agencies to widen their scale of work. However, there is a question on the transparency and accountability of those implementing agencies such as NGOs, and other agencies. On the other hand, Matten and Moon (2008) cited by Bala (2015) mentioned that resources in the form of finance, manpower, and time are the common requirement of CSR projects. Depending upon the availability of resources, companies opt for different modes of executing CSR practices. The manner in which companies actualize social responsibility varies among nations. CSR is varied by context, particularly the context of place or national business systems due to the needs and aspirations of the people and country-specific laws and regulations.

From the findings of the study, it is evident that Schedule (viii) and Schedule (ix) are the least focus sectors/areas. We also witness similar findings from the analysis of the CSR disclosure index where only 10% of companies carried out CSR activities on category H, i.e., contribution to different funds. The companies are not keen on contribution to the Prime Minister's National Relief Fund or any other fund set up by the Central government for socioeconomic development and relief and welfare of the scheduled castes, scheduled tribes, other backward classes, minorities and women that is covered under Schedule (viii) of the Act. It is clear that businesses are less sensitive to dealing with natural catastrophes and other tragedies that our nation encounters. Companies must focus on these issues to fill the gap and support the government in tackling those problems. Today's world is characterized by frequent natural disasters due to several reasons. More businesses should contribute to Schedule (viii) to combat such emergencies and work together with the government and other authorities during an emergency. To mention a few, TATA Foundation, Reliance Foundation, Azim Premji, and many more corporates, philanthropists, and individuals from India and throughout the world's business, sports, and entertainment sectors have donated massive amounts to battle the ongoing Covid-19 pandemic. This act exemplifies India's longstanding relationship with social responsibility, which existed prior to the establishment of mandatory CSR legislation. The company's contribution to 'any other fund set up by the Central government for socioeconomic development and relief and welfare of the scheduled castes, scheduled tribes, other backward classes, minorities, and women' will uplift the socioeconomic status of those groups of people, thereby helping in their equal representation in the socioeconomic and political affairs of the country. To develop the budding entrepreneurs of the country, companies should contribute towards technology incubators in incubating the young budding talents of the country. This will help to develop more entrepreneurs and contribute to the country's economy through technology-enabled entrepreneurship. Companies should provide contributions to the families of combat soldiers who sacrificed their lives for the security of the nation. Those unexplored and untapped sectors/areas should be explored, and corporations' CSR policies should be reframed to include those sectors/areas in their CSR intervention.

CSR is a way to strengthen businesses while contributing to society. To guarantee that required CSR spending is used in other pertinent areas, more initiatives should be undertaken in the fields of art and culture, rural sports, rural development, and disaster management (Mondal and Dhar, 2021). There is also a need to address the disparity in the purposes for which CSR expenditures are made. The government should also take legislative steps to mandate that a proportion of overall expenditure be made for various purposes, and a centralized CSR fund drawing and allocation mechanism should be built to do this. Allocations under the headings of gender equality/women empowerment and encouraging sports, in particular, need to be raised, as the country's performance in these two areas is relatively poor (Das and Ray, 2020).

Conclusion

It may be concluded that the tea companies are serious about CSRD compliances and reporting their CSR activities, but the findings of the study show that the compliance is not satisfactory. It is right time for the tea companies to act on building a trustworthy relationship with the stakeholders. The tea workers should be the focal point considering them as the key stakeholders in CSR implementation. The government should hold dialogues with companies on their CSR priorities and on tea plantation workers as the prime focus of exercising CSR. The study concludes that through CSR reporting, the stakeholders of the company can be made aware of CSR programs. The companies should have greater engagement directly in implementing CSR, which involves interactions and dialogues with stakeholders, and understanding stakeholders' priorities. This in return helps win the trust of the stakeholders through effective stakeholder engagement. As a part of the company's strategy, CSR should emphasize important areas of interaction between key stakeholders and the company to initiate actions that create value (Noked, 2013). CSRD in annual reports is critical for achieving company objectives such as satisfying stakeholders' interests, protecting employees' interests, clarifying the extent of the company's contribution in both CSR activities and CSRD, and assisting investors in making appropriate investment decisions. CSR disclosure has an impact on business performance, including a company's reputation (Bayoud and Kavanagh, 2012).

Limitations and Future Scope: The study is based on limited sample size of 15 tea companies in India. Secondly, the study relied on secondary data available on websites, annual reports, and other company reports. The findings of the study can be only generalized to the tea industry of India and cannot be generalized to other industries. Despite the abovementioned limitations, the study has both theoretical and practical implications. It depicts the present context of CSR practices of the tea companies, provides evidence on CSRD compliance, and the untouched areas of CSR implementation that the government and the companies should focus on effectively and strategically. Further research can be carried out considering more samples using primary data and different methodologies to have a vivid picture of tea companies' CSR intervention. Research may also be undertaken to explore the reasons for noncompliance with the laws requiring CSR disclosure.

References

- Apeejay Tea Limited (n.d.). Retrieved from http://www.apeejaygroup.com/corporatecitizenship.html

- APPL Foundation (n.d.). Retrieved from Amalgamated Plantations: https://applfoundation.in/

- B&A Limited (n.d.). Retrieved from B & A Limited: https://www.barooahs.com/

- Bala M (2015), "A Comparative Study of Methods of CSR Implementation in Indian Context", International Journal of Management, Vol. 6, No. 1, pp. 5-18.

- Banerji S and Willoughby R (2019), "Addressing the Human Cost of Assam Tea: An Agenda for Change to Respect", Protect and Fulfil Human Rights on Assam Tea Plantations, Oxfam GB for Oxfam International, doi:10.21201/2019.4870.

- Baskin J and Gordon K (2005), "Corporate Responsibility Practices of Emerging Market Companies", OECD Working Papers on International Investment, [online] doi:10.1787/713775068163.

- Bayoud N S and Kavanagh M (2012), "Corporate Social Responsibility Disclosure: Evidence from Libyan Managers", Global Journal of Business Research, [online], Vol. 6, No. 5, pp. 73-83, http://www.theibfr2.com/RePEc/ibf/gjbres/gjbr-v6n5-2012/GJBR-V6N5-2012-6.pdf. Accessed on December 22, 2022.

- Bengal Tea and Fabrics Ltd. (n.d.). Retrieved from http://bengaltea.com/

- Bhatia A and Chander S (2014), "Corporate Social Responsibility Disclosure by SENSEX Companies in India", Management and Labour Studies, Vol. 39, No. 1, pp. 1-17, doi:10.1177/0258042x14535161.

- Bora P P (2015), "Corporate Social Responsibility Norms and Tea Industry in Assam", Dimorian Review, Vol. 5, No. 2, pp. 17-26.

- Bosumatari D and Goyari P (2013), "Educational Status of Tea Plantation Women Workers in Assam: An Empirical Analysis", Asian Journal of Multidisciplinary Studies, [online] Vol. 1, No. 3, pp. 17-26, https://core.ac.uk/download/pdf/229682615.pdf. Accessed on December 22, 2022.

- Chakraborty V (2019), Climate Change, Worker's Rights and Tea Industry in Assam: An Analysis, Vol. 5, No. 5, pp.166-178, Law Brigade (Publishing) Group.

- Chaudhary U K and Chaudhary M (2014), "Disclosure of Interest and Related Party Transactions: Some Intricate Issues", The Journal for Corporate Professionals, [online] Vol. 44, No. 7, pp. 825-984, https://www.icsi.edu/media/webmodules/linksofweeks/JulyCS_2014.pdf?

- Chaudhri V and Jian Wang (2007), "Communicating Corporate Social Responsibility on the Internet", Management Communication Quarterly, [online] Vol. 21, No. 2, pp. 232-247, doi:10.1177/0893318907308746.

- Chen Y C, Hung M and Wang Y (2018), "The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China", Journal of Accounting and Economics, Vol. 65, No. 1, pp. 169-190, doi:10.1016/j.jacceco. 2017.11.009.

- Dagiliene L (2010), "The Research of Corporate Social Responsibility Disclosures in Annual Reports", Inzinerine Ekonomika-Engineering Economics, Vol. 21, No. 2, pp. 197-204.

- Darjeeling Organic Tea Estates Pvt. Ltd. (n.d.). Retrieved from Darjeeling Organic Tea Estates Pvt. Ltd., http://www.dotepl.com/our-story/sustainability

- Das Gupta A M S (2017), "Improving Labour Productivity through Human Resource Development: A Case Study on Assam Tea Plantation Workers", Journal of Supply Chain Management Systems, Vol. 6, No. 1, pp. 8-22.

- Das S and Ray P (2020), "Empirical Study on Equity in Csr Spending: With Special Reference to India", EPRA International Journal of Multidisciplinary Research (IJMR), Vol. 6, No. 7, pp. 367-373, doi:10.36713/epra2013.

- Datta S and Karande V (2017), "Whither Strategic or Responsive CSR: Evidences from Indian Companies with Reference to Public Disclosures under Companies Act 2013", Work in Progress.

- Desai N, Farrell M, Grajales A et al. (2018), "Corporate Social Responsibility and Women's Empowerment: Best Practices and Case Studies", School of International and Public Affairs.

- Dhaneshwar A and Pandey P (2015), "Status of Corporate Social Responsibility among PSUs in India", India Environment Portal.

- Dhunseri Tea & Industries Limited. (n.d.), Retrieved from https://dhunseritea.com/

- Duara M and Mallick S (2019), "Women Workers and Industrial Relations in Tea Estates of Assam Handloom as a Sustainable Socio-Technological System: A Study of Textile Industry in North-East India View project Mridusmita Duara", The Indian Journal of Industrial Relations, Vol. 55, No. 1, pp. 15-26.

- Dutta A and Basu R (2017), "Status of Household Food Security in the Tea Gardens of Jalpaiguri District in West Bengal, India", IOSR Journal of Humanities and Social Science (IOSR-JHSS), [online] Vol. 22, No. 9, pp. 49-57, doi:10.9790/0837-220901 4957.

- Dyduch J and Krasodomska J (2017), "Determinants of Corporate Social Responsibility Disclosure: An Empirical Study of Polish Listed Companies", Sustainability, Vol. 9, No. 11, p. 1934, doi:10.3390/su9111934.

- Ehsan S, Nazir M, Nurunnabi M et al. (2018), "A Multimethod Approach to Assess and Measure Corporate Social Responsibility Disclosure and Practices in a Developing Economy", Sustainability, Vol. 10, No. 8, p. 2955, doi:10.3390/su10082955.

- Ganesan J and Saravanabavan V (2018), "Nutritional Problems of Anaemia Disorders Among the Tea Plantation Labourers in Nilgiris District: A Geo Medical Study Nutritional Problems of Anaemia Disorders Among the Tea Plantation Labourers in Nilgiris District-A Geo Medical Study", IJSRSET, Vol. 4, No. 4,pp. 1360-1366.

- Goodricke Group. (n.d.). Retrieved from https://www.goodricke.com/

- Goowalla H (2014), "Corporate Social Responsibility Towards the Workers in Tea Industry of Assam - A Case Study With Special Reference to Three Company Based Industry, International Journal of Research-granthaalayah, Vol. 2, No. 2, pp. 14-19. doi:10.29121/granthaalayah.v2.i2.2014.3063.

- Grob Tea Co. Ltd. (n.d.). Retrieved from http://www.grobtea.com/

- Gujarat Tea Processors & Packers Ltd. (n.d.). Retrieved from https://www.wagh bakritea.com/contact-us.php

- Gunathilaka R P D and Tularam G A (2016), "The Tea Industry and a Review of Its Price Modelling in Major Tea Producing Countries Water security in Sub-Saharan Africa View Project Impact of Climate Variability on Perennial Crop Production and Profitability: The Case of Tea Production in Sri Lanka View Project", Journal of Management and Strategy, Vol. 7, No. 1, http://jms.sciedupress.com. doi:10.5430/jms.v7n1p21.

- Gurung M and Mukherjee S R (2018), "Gender, Women and Work in the Tea Plantation: A Case Study of Darjeeling Hills", The Indian Journal of Labour Economics, Vol. 61, No. 3, pp. 537-553, doi:10.1007/s41027-018-0142-3.

- Haldar P K (2015), "The Changing Facets of Corporate Governance and Corporate Social Responsibilities in India and their Interrelationship", Information Management and Business Review, Vol. 7, No. 3, pp. 6-16, doi:10.22610/imbr.v7i3.1148.

- Hassan Nasr Taha (2010), "Corporate Social Responsibility Disclosure:an Examination of Framework of Determinants and Consequences", Durham Theses, Durham University, Durham E-Theses Online: http://etheses.dur.ac.uk/480/

- Hazarika K (2011), "Changing Market Scenario for Indian Tea", International Journal of Trade, Economics and Finance, Vol. 2, No. 4, p. 285.

- Henkel Ramon E (1976), Tests of Significance, Sage University Paper Series on Quantitative Applications in the Social Sciences, 07-004, Sage, Newbury Park, CA.

- Islam T, Ali G, Aziz A et al. (2018), "Employees' Response to CSR: Role of Organizational Identification and Organizational Trust", Pakistan Journal of Commerce and Social Sciences, [online] Vol. 12, No. 1, pp. 153-166, http://jespk.net/publications/418.pdf. Accessed on December 22, 2022.

- Jain M (2015), "Is Companies Act, 2013 Forcing Corporate to do Charity?: A Critical Analysis of CSR Regime of New Corporate Legislature of India", International Journal of Multidisciplinary Approach and Studies, [online] Vol. 2, No. 2, http://dspace.stellamariscollege.edu.in:8080/xmlui/bitstream/handle/123456789/7975/CSR.pdf?sequence=1&isAllowed=y. Accessed on December 22, 2022.

- Jarwal D And Kahal A (2021), "An Analysis of Marginal Benefits of Corporate Social Responsibility Expenditures in India", Ruminations, Vol. 12, No. 2, pp. 151-175.

- Kadavil S M (2005), Indian Tea Research, SOMO, The Netherlands.

- Khawas V (2011), "Status of Tea Garden Labourers in Eastern Himalaya: A Case of Darjeeling Tea Industry, Cloud, Stone and the Mind: The People and Environment of Darjeeling Hill Area", KP Bagchi & Company, India.

- Krippendorff K (1989), "Content Analysis", in E Barnouw G Gerbner W Schramm, T L Worth and L Gross (Eds.), International Encyclopedia of Communication, Vol. 1, pp. 403-407, Oxford University Press, New York. Retrieved from http://repository.upenn.edu/asc_papers/226

- Lebaron G (2021), "Wages: An Overlooked Dimension of Business and Human Rights in Global Supply Chains", Business and Human Rights Journal, Vol. 6, No. 1, pp. 1-20, doi:10.1017/bhj.2020.32.

- Madhu Jayanti International Limited. (n.d.). Retrieved from http://www.jaytea.com/

- Mahadevappa B and Rechanna S (2012), Corporate Social Reporting Practices in India.

- Mcleod Russel Limited. (n.d.). Retrieved from Mcleod Russel Limited: https://www.mcleodrussel.com/

- Michaels A and Gruning M (2018), "The Impact of Corporate Identity on Corporate Social Responsibility Disclosure", International Journal of Corporate Social Responsibility, Vol. 3, No. 1, doi:10.1186/s40991-018-0028-1.

- Ministry of Corporate Affairs - Government of India (2014), February 27. Retrieved from https://www.mca.gov.in/Ministry/pdf/CompaniesActNotification3_2014.pdf

- Ministry of Corporate Affairs - Government of India (n.d.). Retrieved from www.mca.gov.in/Ministry/pdf/InvitationOfPublicCommentsHLC_18012019.pdf

- Ministry of Corporate Affairs (2014), February 27. Retrieved from https://www.mca.gov.in/Ministry/pdf/CompaniesActNotification3_2014.pdf

- Ministry of Labour & Employment, Government of India (1951), "The Plantations Labour Act, 1951" [online] https://labour.gov.in/sites/default/files/The-Plantation-Labour-Act-1951.pdf. Accessed on December 22, 2022.

- Mondal T and Dhar S (2021), "Mandatory Corporate Social Responsibility Expenditure in India: Analysis of Practice of Selected Large Companies", International Journal of Advanced Research in Commerce, Management & Social Science, Vol. 4, No. 4, pp.189-197.

- National CSR Portal. (n.d.). Home [online], https://csr.gov.in/content/csr/global/master/home/home.html.

- Noked N (2013), "The Corporate Social Responsibility Report and Effective Stakeholder Engagement" [online] Harvard.edu, https://corpgov.law.harvard.edu/2013/12/28/the-corporate-social-responsibility-report-and-effective-stakeholder-engagement

- Platonova E, Asutay M, Dixon R and Mohammad S (2016), "The Impact of Corporate Social Responsibility Disclosure on Financial Performance: Evidence from the GCC Islamic Banking Sector", Journal of Business Ethics, Vol. 151, No. 2, pp. 451-471, doi: 10.1007/s10551-016-3229-0.

- Pradhan S and Ranjan A (2011), "Corporate Social Responsibility in Rural Development Sector: Evidences from India", School of Doctoral Studies (European Union) Journal, Vol. 2, pp. 139-147.

- Rafeeque A and Sumathy N (2021), "A Study on Problem Faced by The Tea Plantation Women Workers in Wayanad District Pjaee", PalArch's Journal of Archaeology of Egypt/Egyptology, Vol. 18, No. 4.

- Ranjan R and Tiwary P K (2018), "A Comparative Study of CSR in Selected Indian Public & Private Sector Organisations in Globalisation Period: A Research Finding", International Journal of Emerging Research in Management and Technology, Vol. 6, No. 6, pp. 270-277, doi:10.23956/ijermt.v6i6.281.

- Saha D, Bhue C and Singha R (2019), "Decent Work for Tea Plantation Workers in Assam: Constraints, Challenges and Prospects", Tata Institute of Social Sciences, Guwahati Campus.

- Saha P (n.d.), "An Analysis of the Patterns of CSR Reporting Practices of Indian MNCs", Business Studies, p. 156.

- Sarabu V (2017), "Corporate Social Responsibility in India: An Over View", Journal of Asian Business Management, Vol. 9, No. 1, pp. 53-67.

- Sarkar S and Bhuvanendran R (2019), "A Cup Full of Woes: Wages & Tea Industry A Cup Full of Woes: Wages and Tea Industry", Indian Journal of Economics and Development, Vol. 7, No. 2.

- Sarma S (2019), "Missing Daughters of the East: Tea Gardens and its Disappearing Women Population", IOSR Journal of Humanities and Social Science (IOSR-JHSS), Vol. 24, No. 2, pp. 24-27, doi:10.9790/0837-2402052427.

- Sharma S (2013), "A 360 Degree Analysis of Corporate Social Responsibility (CSR) Mandate of the New Companies Act, 2013", Global Journal of Management and Business Studies, [online] Vol. 3, No. 7, pp. 757-762, https://www.ripublication.com/gjmbs_spl/gjmbsv3n7_09.pdf . Accessed on December 23, 2022.

- Singh R and Agarwal S (2013), "Corporate Social Responsibility for Social Impact: Approach to Measure Social Impact using CSR Impact Index", Indian Institute of Management Calcutta, 729.

- Soares L, Wanderley O, Lucian R et al. (2008), "CSR Information Disclosure on the Web: A Context-Based Approach Analysing the Influence of Country of Origin and Industry Sector", Journal of Business Ethics, Vol. 82, No. 2, pp. 369-378, doi:10.1007/sl0551-008-9892-z.

- Soltani E, Syed J, Liao Y Y and Iqbal A (2014), "Managerial Mindsets Toward Corporate Social Responsibility: The Case of Auto Industry in Iran", Journal of Business Ethics, Vol. 129, No. 4, pp. 795-810, doi:10.1007/s10551-014-2137-4.

- Stemler S (2000), "An Overview of Content Analysis, Practical Assessment, Research, and Evaluation", [online] Vol. 7, No. 17, pp.1531-7714, https://scholarworks.umass.edu/cgi/viewcontent.cgi?article=1100&context=pare

- Stemler S E (2015), "Content Analysis", Emerging Trends in the Social and Behavioral Sciences, pp. 1-14, doi:10.1002/9781118900772.etrds0053.

- Sufian M (2012), "Corporate Social Responsibility Disclosure in Bangladesh Corporate Social Responsibility Disclosure in Bangladesh", Global Journal of Management and Business Research, Vol. 12, No. 14.

- Sumitha S (2012), "Bringing in, Living In, Falling Out: Labour Market Transitions of Indian Plantation Sector", A Survey, pp. 5-51.

- Thacker H (2019), "CSR: Price of a Cup of Tea", [online] The CSR Journal, https://thecsrjournal.in/csr-price-of-a-cup-of-tea/. Accessed on December 23, 2022.

- The United Nilgiri Tea Estates Company Limited (n.d.). Retrieved from https://unitednilgiritea.com/?page_id=41

- Tirkey L and Nepal P (2012), "Tea Plantations in the Darjeeling Hills Geo-Ecological Impact and Livelihood Implications", Journal of Water, Energy and Environment, Hydro Nepal, Vol. 10, pp. 53-59.

- Vijayabaskar M and Viswanathan P (2019), "Emerging Vulnerabilities in India's Tea Plantation Economy: A Critical Engagement with Policy Response", Mids Madras Institute of Development Studies.

- Warren Tea Limited. (n.d.). Retrieved from Warren Tea Limited, https://www.warrentea.com/

- Wijerathna I and Gajanayaka R (2014), "The Socio-Economic Impact of Corporate Social Responsibility Practices in Sri Lankan Tea Manufacturing Companies (Special Reference to Kandy District)", Kelaniya Journal of Management, Vol. 2, No. 1, p. 113, doi:10.4038/kjm.v2i1.6546.

- Worokinasih S and Zaini M (2020), "The Mediating Role of Corporate Social Responsibility (CSR) Disclosure on Good Corporate Governance (GCG) and Firm Value, A Technical Note", Australasian Accounting, Business and Finance Journal, Vol. 14, No. 1, pp. 88-96, doi:10.14453/aabfj.v14i1.9.