Jan'23

The IUP Journal of Organizational Behavior

Archives

Occupational Stress Among Accounting Professionals: A Systematic Literature Review

Nisha

Research Scholar, Dept. of Commerce, Central University of Haryana, Haryana, India.

E-mail: nishamoar24@gmail.com

The objective of the study is to systematically review the literature pertaining to occupational stress among accounting professionals. Although occupational stress is a much-talked about phenomenon, managers have not been able to solve the problem effectively. Therefore, to comprehend the complex and holistic nature of the phenomenon, a review of literature available from 1985 to 2020 was carried out using different databases. Personal factors that induce stress such as locus of control, work-home conflict, social support, personality and gender were studied extensively. The review provides an objective understanding of the research status in this extremely significant field and helps in identifying the research gap and key domains for future research and/or theory development.

Introduction

Occupational stress has become an integral part of an employee's professional life. If remained unchecked, stress can have various effects on the performance of the employee as well as his physical and mental health. It has different impact on not only his professional but also his personal life. It may have various psychological, physiological and behavioral consequences. Digging further into the psychological wellbeing of the employee at the workplace, it is contended that the burden on the employees is strongly related to worsening psychological health (Stevenson and Farmer, 2017). Organizations are finding it difficult to improve the productivity of the employees who are not able to perform to their full potential because of their mental health. Therefore, there is a need for transformation on the professional front, which leads to the question as to how to equip the workforce to deal with stress at work in a better way.

In a study conducted by the Institute of Directors (Silvester, 2017), only about 14% organizations have any kind of policy or training for stress management, in spite of the possible effects of stress and mental wellbeing on the productivity of employees. This suggests that a lot has to be done to contain the problem of stress. Therefore, organizations must deal with the problem effectively as poor mental health of the employees may lead to poor decision-making and increase in conflicts and turnover among employees (Silvester, 2017).

Many organizations have proposed ways to mitigate stress at workplace. However, a common approach towards management of stress might not be successful as the industries are different, and the nature of work also differs. Reduction in stress may provide practical solutions to improve productivity and efficiency. Many studies have claimed that high stress levels significantly affect productivity (Okeke et al., 2016). However, this relationship was further bolstered by Richardson (2014), who linked stress to productiveness of the employee.

Previous studies have offered suggestions on how to deal with role stressors in the organization (Fisher, 2001; and Viator, 2001). Nevertheless, some opportunities are available to modify the stress-causing factors found in the work environment of public accounting at the individual level. Prior studies draw attention to the probable impact of extreme stress and burnout in various professions, studying the causes of stress and its outcomes (e.g., Goolsby, 1992; Schiltz and Syverud, 1999; Fogarty et al., 2000; and Williams et al., 2001).

Why Study Occupational Stress Among Accounting Professionals?

Accountants work long hours every day to ensure that they achieve their deadlines. Stress at work is a negative physiological and psychological reaction that arises when an individual's personal capabilities or talents are not sufficient to meet the requirements of the position. This causes the individual to feel pressure and anxiety about their ability to succeed in the position. Accounting professionals have to keep themselves updated with the constantly changing accounting rules and regulations to hold on to their jobs. With the advent of globalization and the organizations going multinational, this has become even more difficult for them as there are several international accounting standards to be followed by them. Studies related to accountants and auditors have been chosen for the review, as the profession is very dynamic and there is a lot of stress.

While many professionals are constantly under pressure, the different qualities associated with the work of public accounting leads to the more difficult circumstances of an accounting professional. Firstly, accountants have to face "busy season," when they usually deal with extreme stress as they have to meet tight deadlines, causing work-family conflict and leaving very less time for relaxation during this time period (Sanders et al., 1995; and Fogarty et al., 2000). Secondly, increase in capital market activity over the years and the economic downturn, command continuous consideration towards professional as well as legal protocols (Lee, 2007). Thirdly, entry-level personnel or interns have to prepare for the chartered accountant exam, which must be cleared to continue working as a public accountant (Carpenter and Hock, 2008). Fourthly, public accountants tend to bring home work-related stress, which results in further inter-personal stress (Figler, 1980).

Stress has been a topic of apprehension among the accountants since Friedman

et al. (1958) recognized the variations in their chemistry of blood prior to and post the "busy" season. They accredited those variations to the stress experienced by the accountants during that time of the year. Over the subsequent years, too many studies have been conducted with respect to stress among accounting professionals which included a considerable number of studies regarding the antecedents and the outcomes of stress.

The studies conducted in the past years in the area of accounting claim the relation between numerous stress-causing factors and outcomes of such stress in a public accounting environment (e.g., Sorensen and Sorensen, 1974; Choo, 1986; Rebele and Michaels, 1990; Collins and Killough, 1989; 1992; Fisher, 2001; and Sweeney and Summers, 2002). Job burnout is the outcome of the snowball effect of stress-causing factors which when experienced can overpower the coping strategies of the employee (Feldman and Weitz, 1988).

Many significant studies have been conducted in the area of occupational stress. However, the question of how to measure the stress level in accounting professionals and reduce its impact on employees remains unresolved. Also, there might be some unexplored factors that may affect the level of occupational stress. Therefore, the field requires a lot of attention of the researchers as there are lots of possibilities for empirical as well as conceptual research.

Data and Methodology

The aim of the study is to obtain objective and reliable knowledge of stress in an accurate manner. This study, with the help of systematic literature review, tries to have an insight on the occupational stress among employees of accounting firms. The study is not confined to specific contexts with their variables. It considers all the stressors in accounting professionals and tries to identify the appropriate factors which increase the level of stress and the variables which have not been studied in depth in the past but may be of utmost importance. A total of 52 research papers were selected for the review of literature based on inclusion and exclusion criteria. The small number of papers to be considered is because of the very narrow inclusion criteria.

Keywords such as "organizational stress", "occupational stress among accountants", "accounting professionals", "stress in organizations", and "stress among men and women", with publication "between 1985 and present" were used for the search in various databases and Google Scholar, including Emerald Insight, Taylor and Francis, Springer, Cambridge Journals and ScienceDirect.

Inclusion and Exclusion Criteria

The criteria for the selection of papers for the study are:

1. Occupational stress among accounting professionals must be a significant variable in the study showing a direct relationship between occupational stress and its outcomes and the antecedent variables of stress and occupational stress.

2. The papers/articles were required to have sufficient number of references in order to warrant the study's scholastic aptitude.

3. The study must have been carried out between 1985 and 2021.

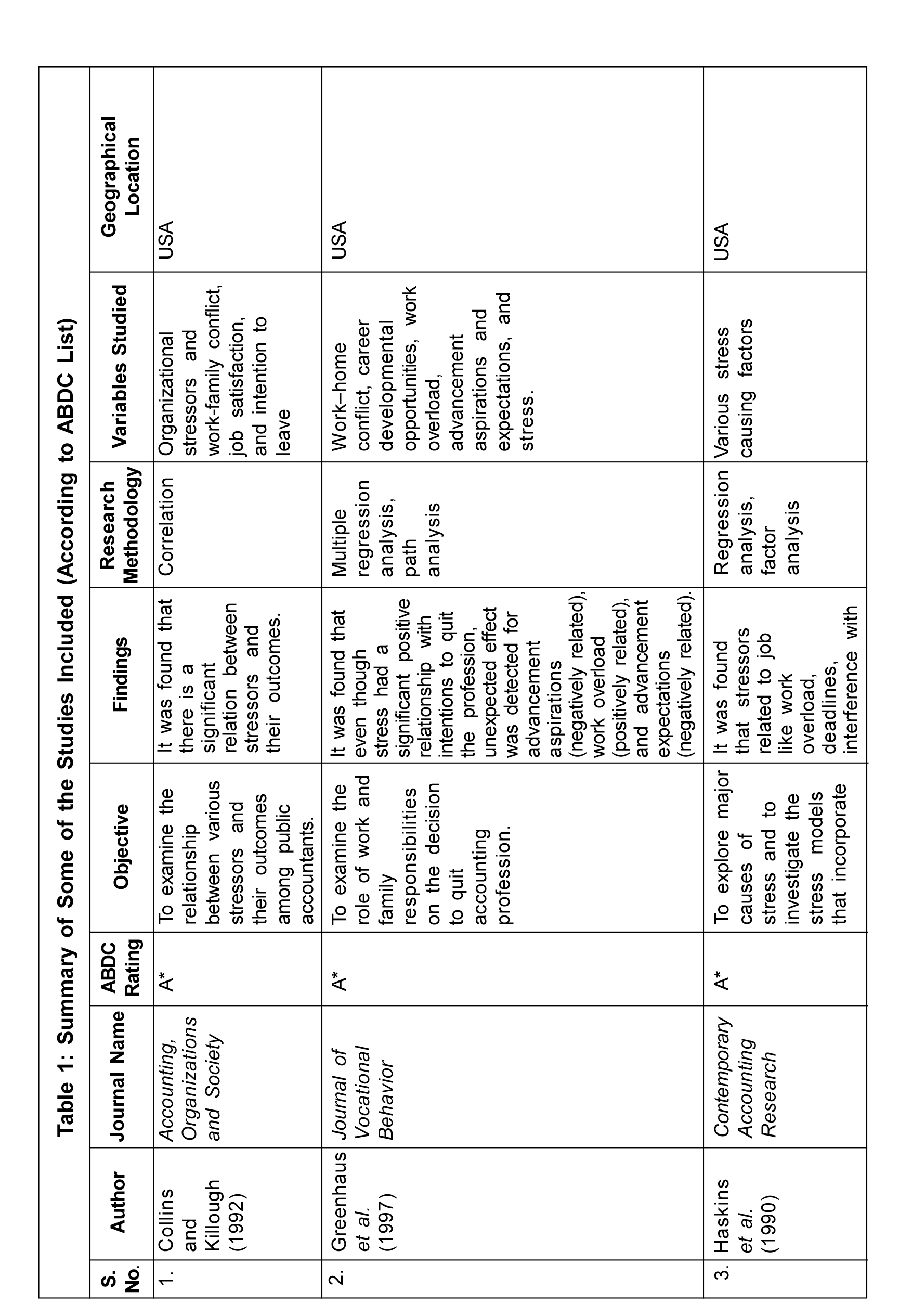

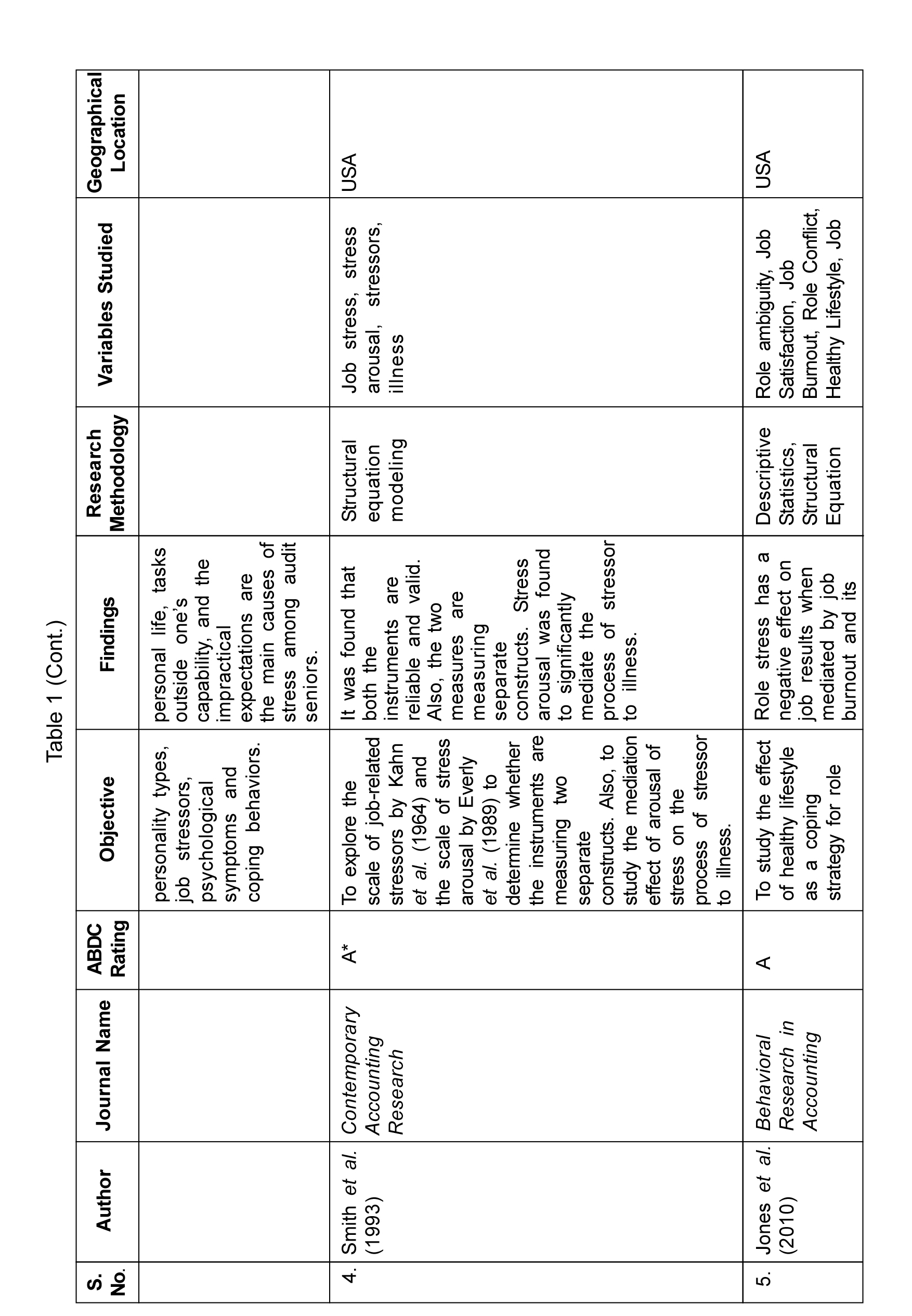

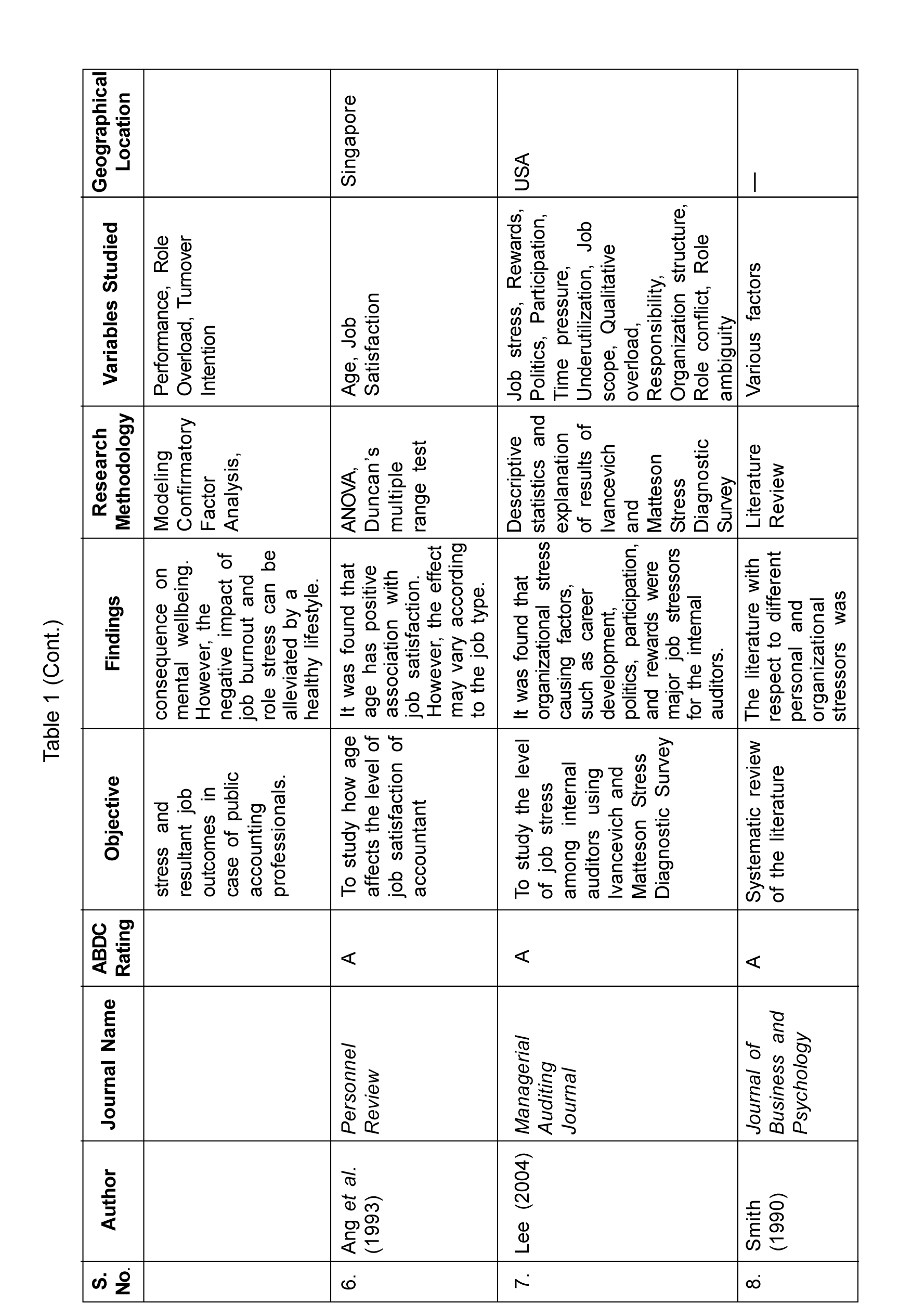

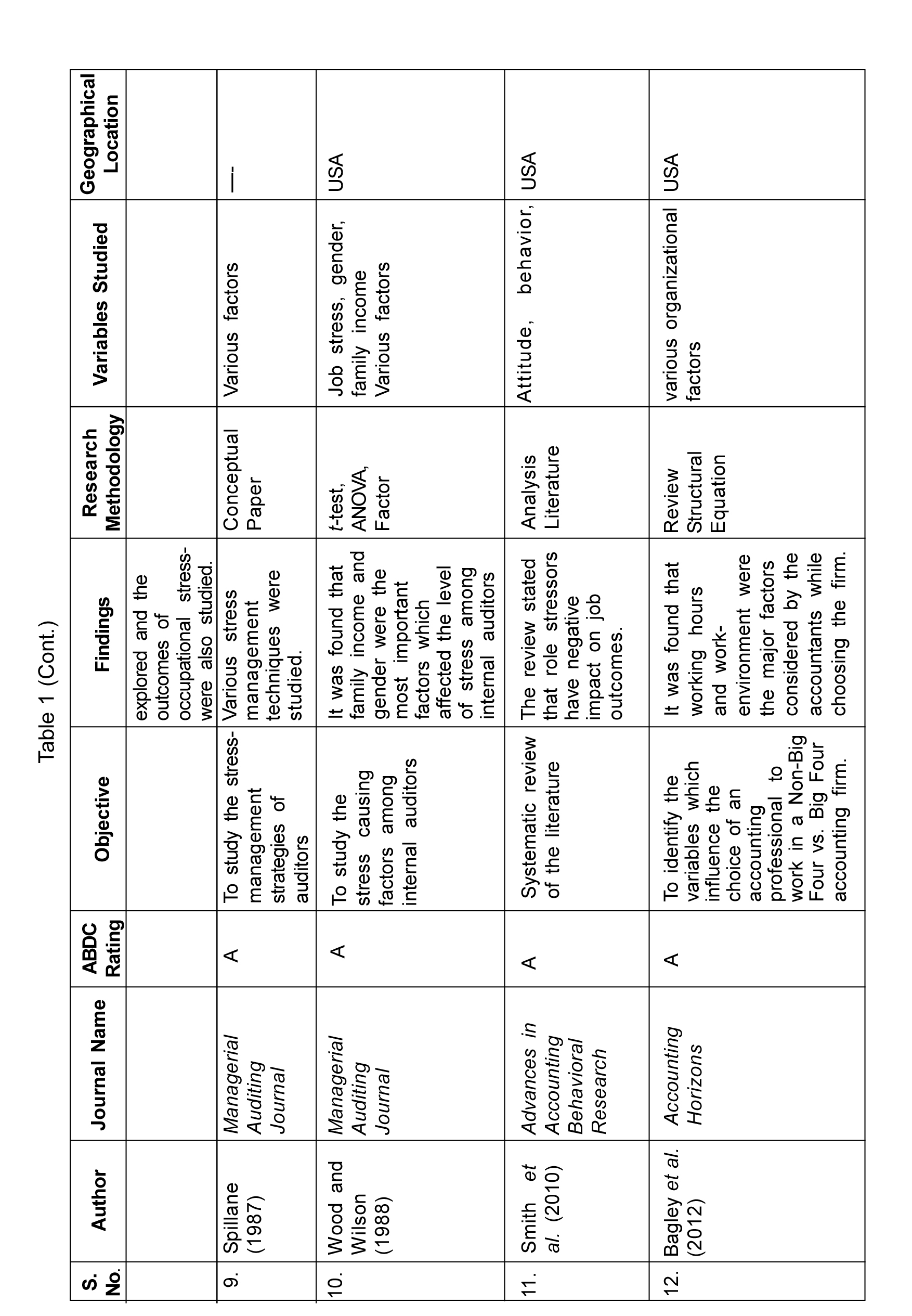

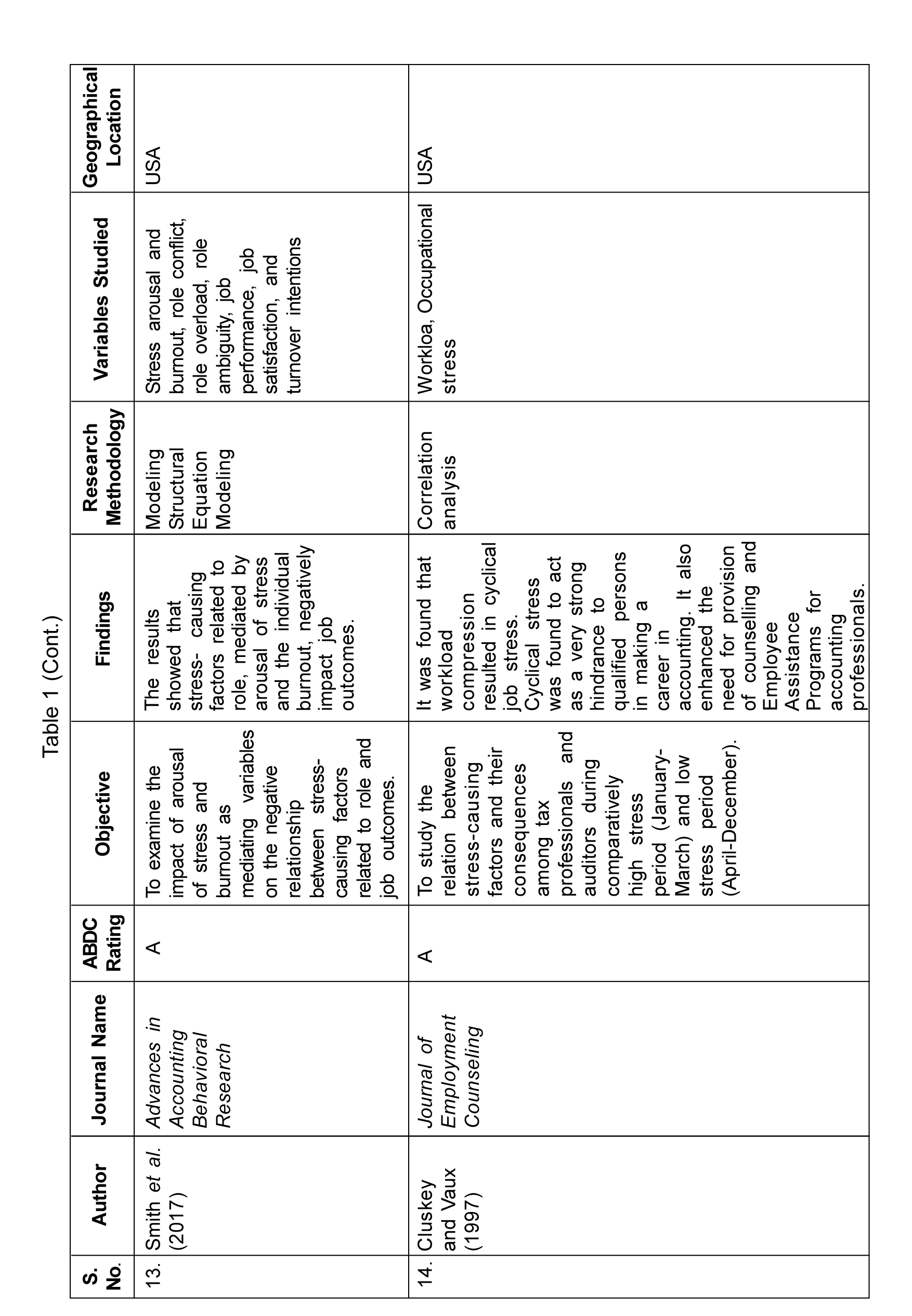

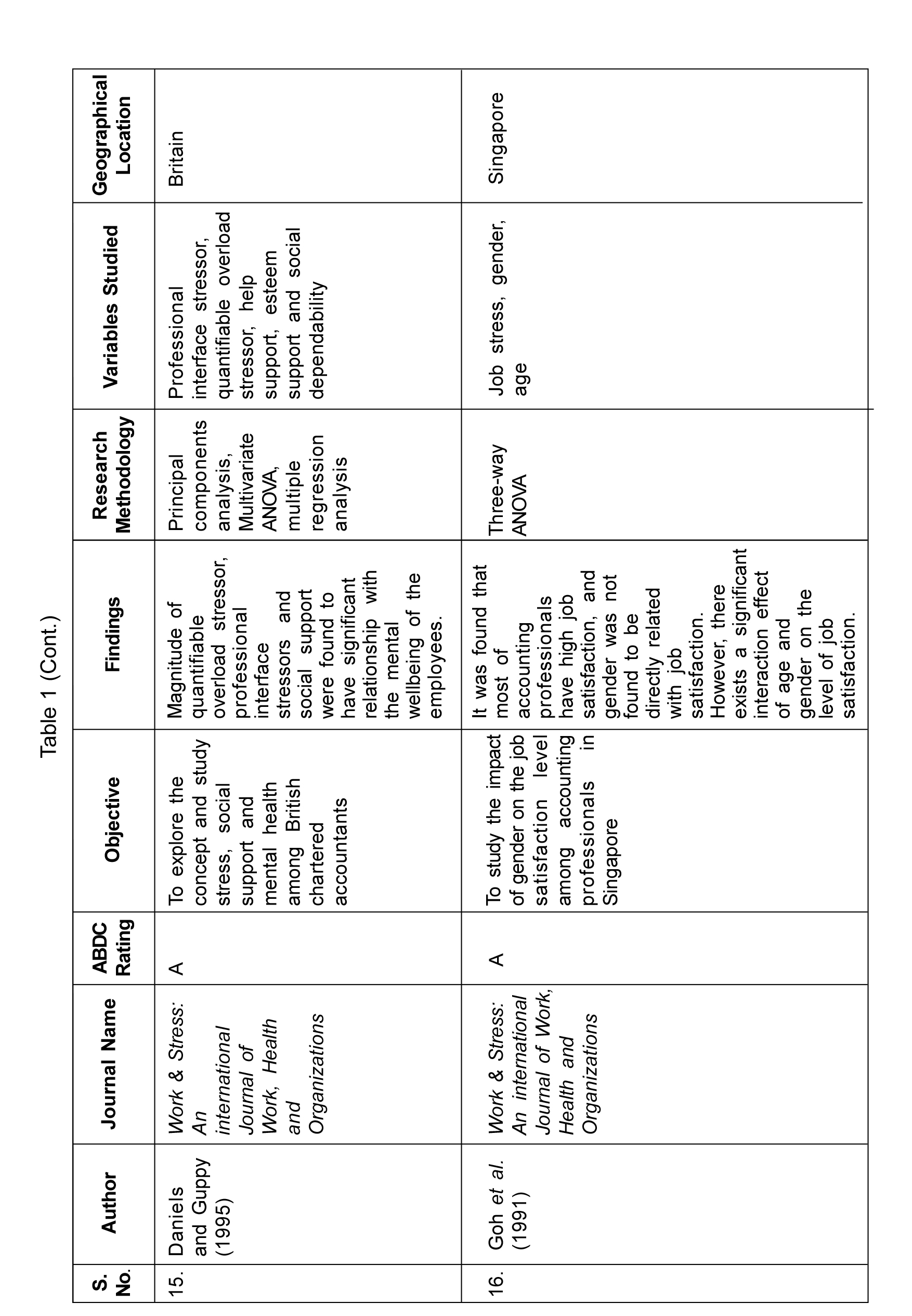

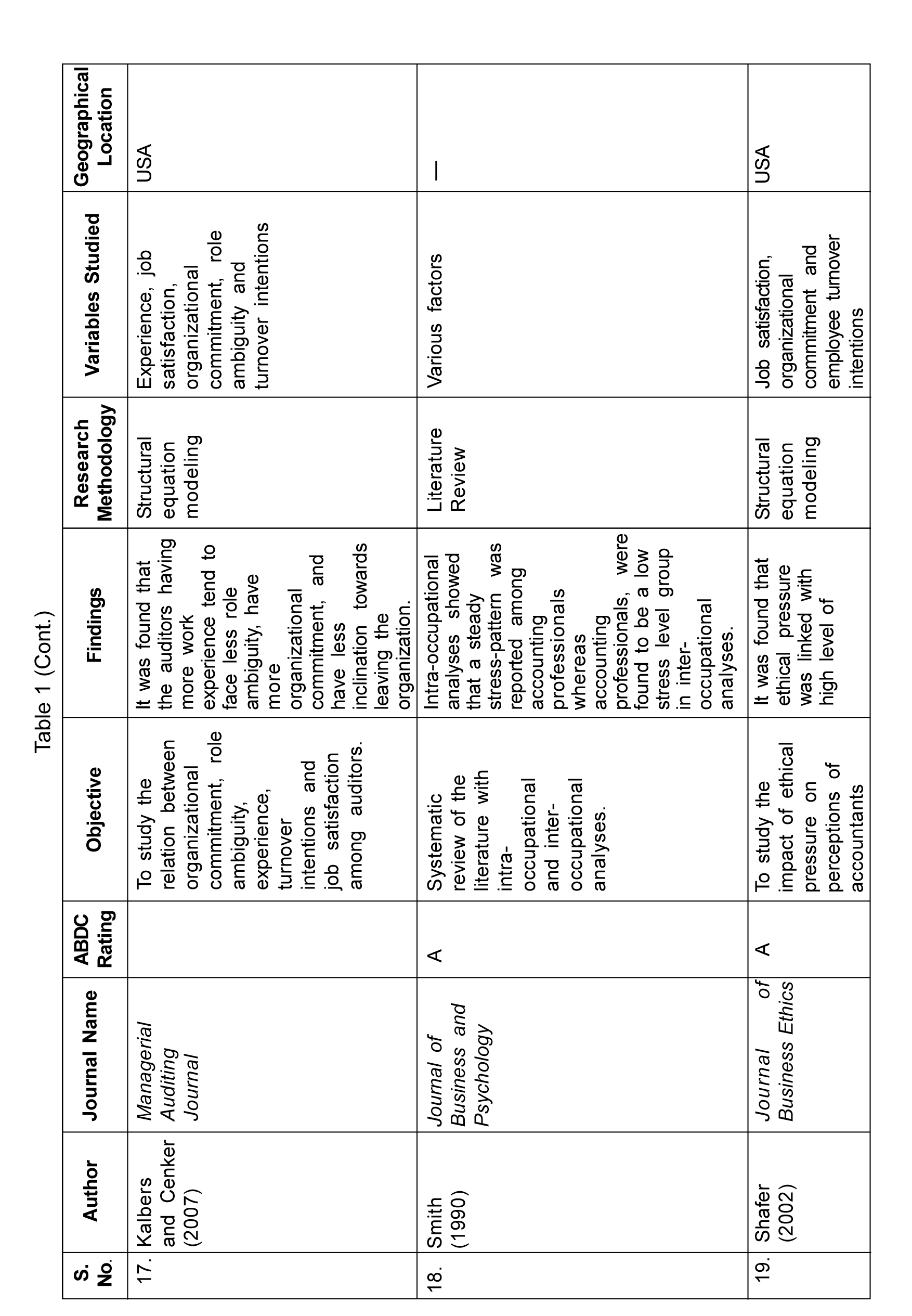

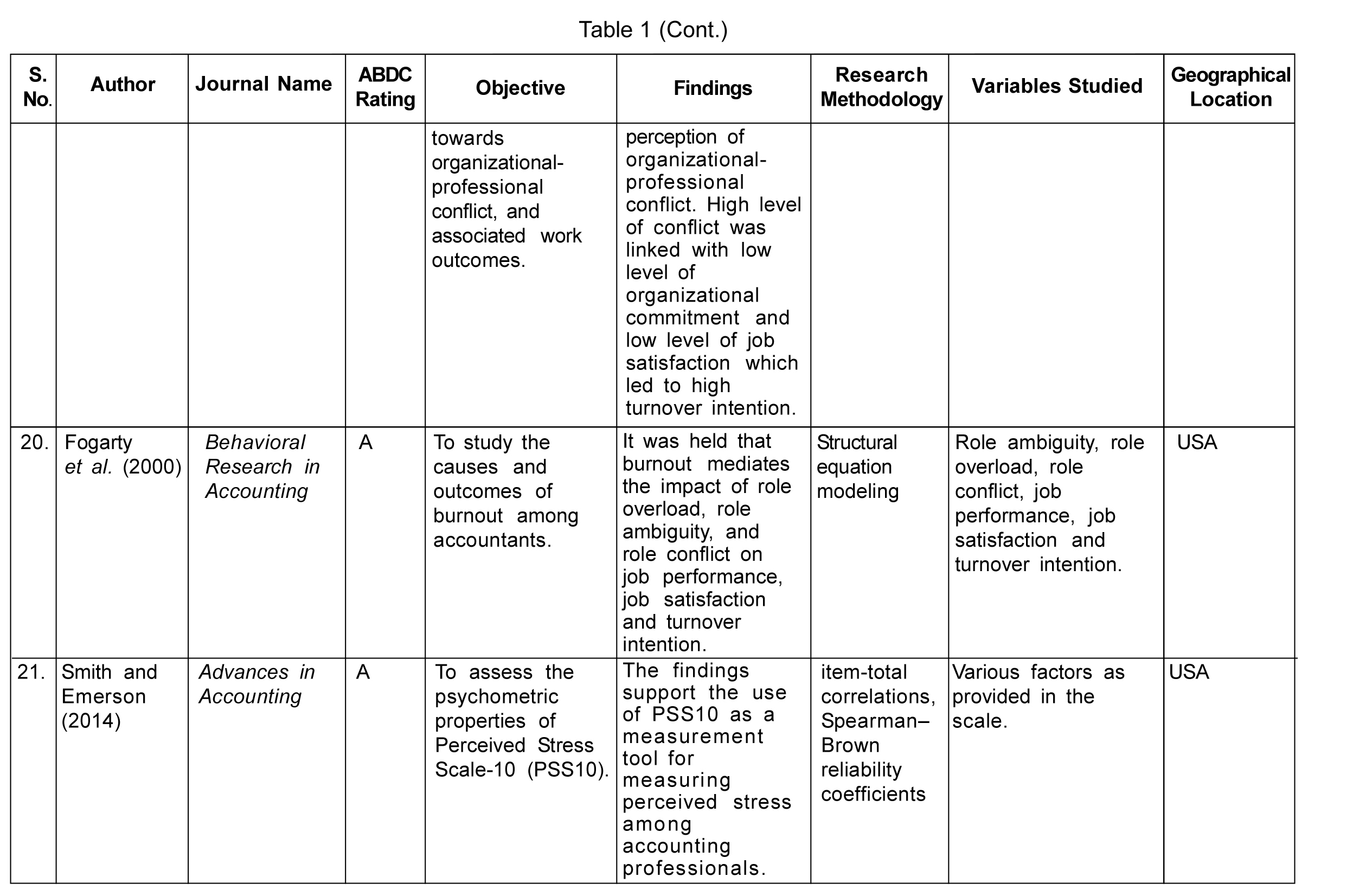

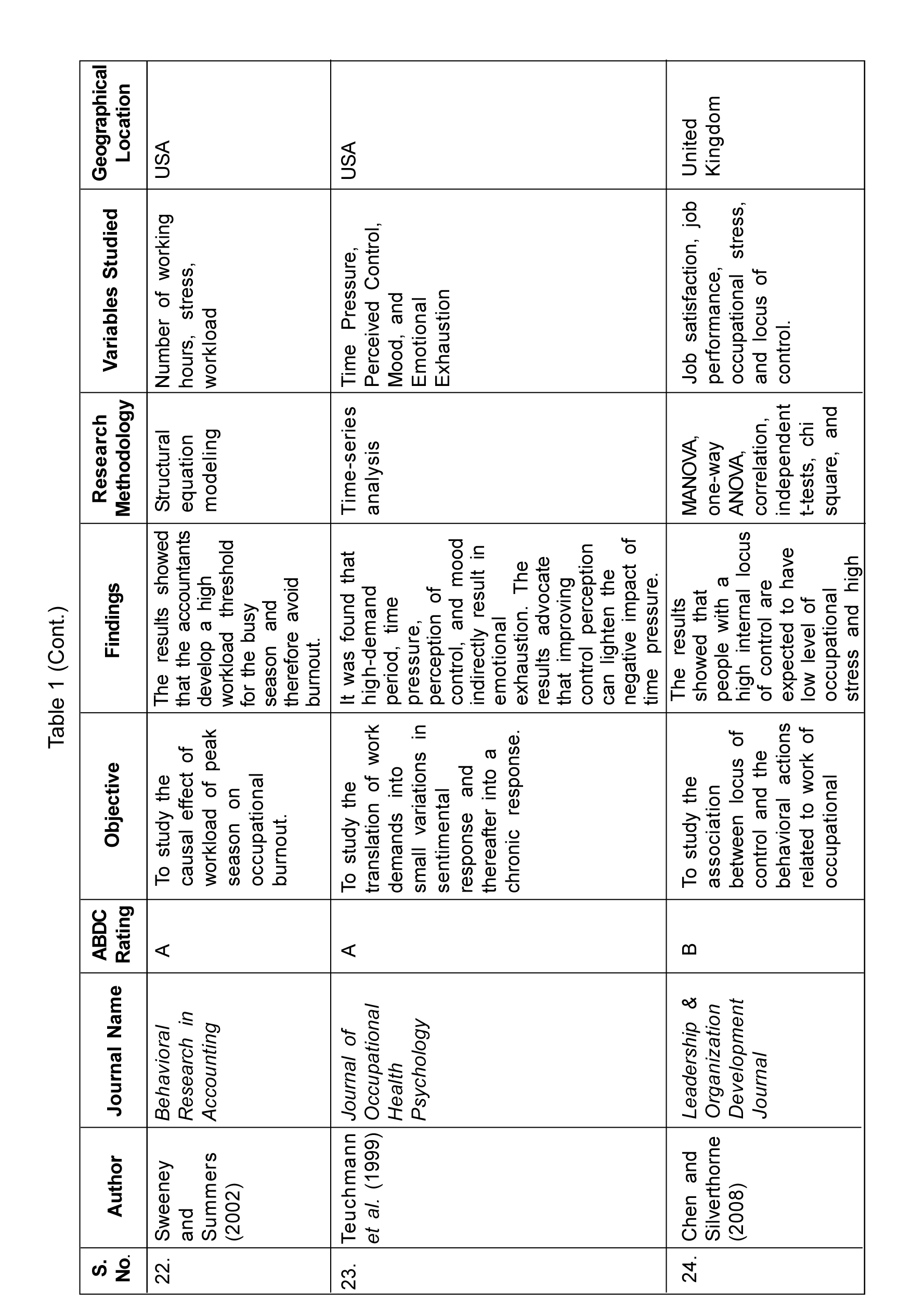

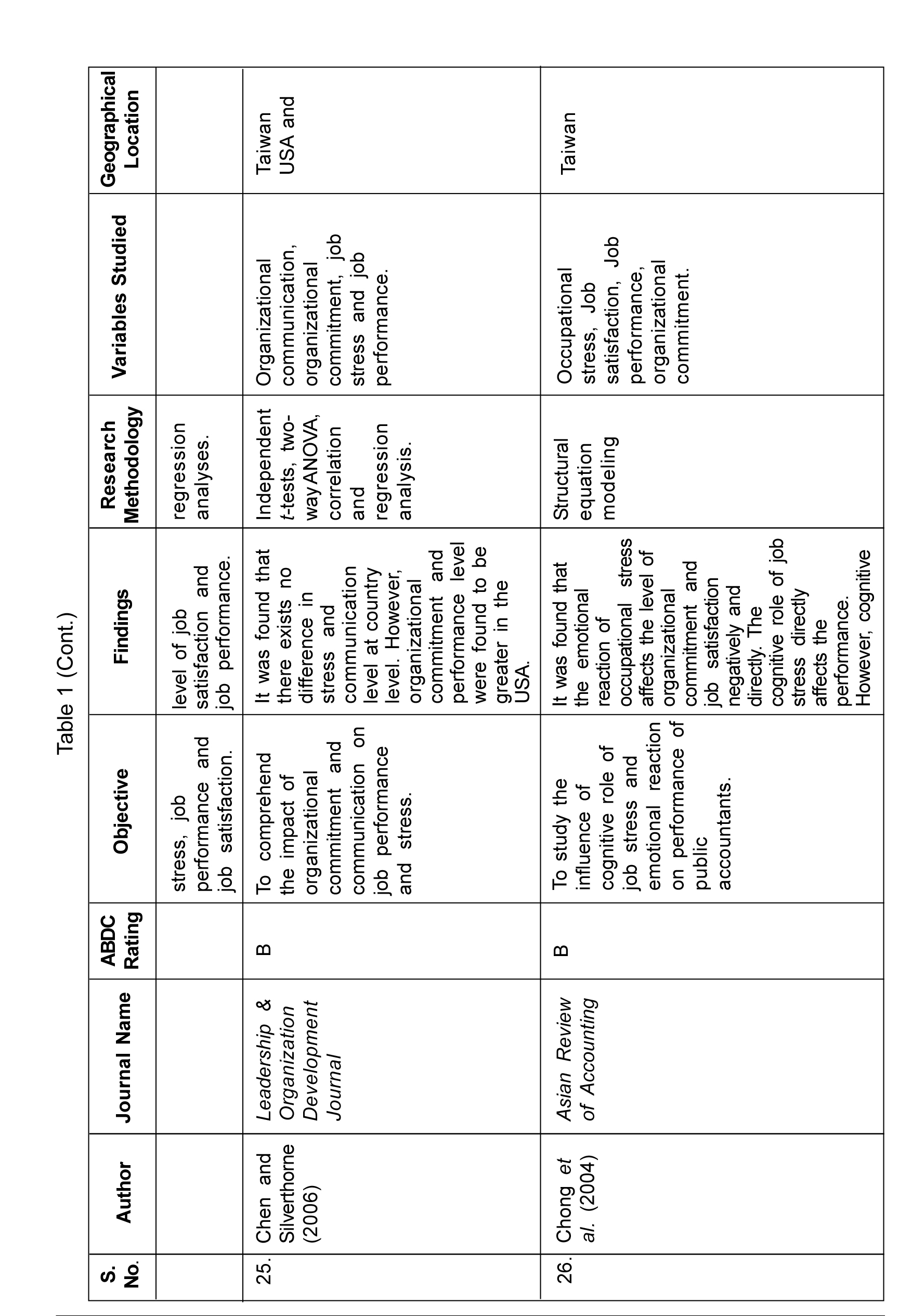

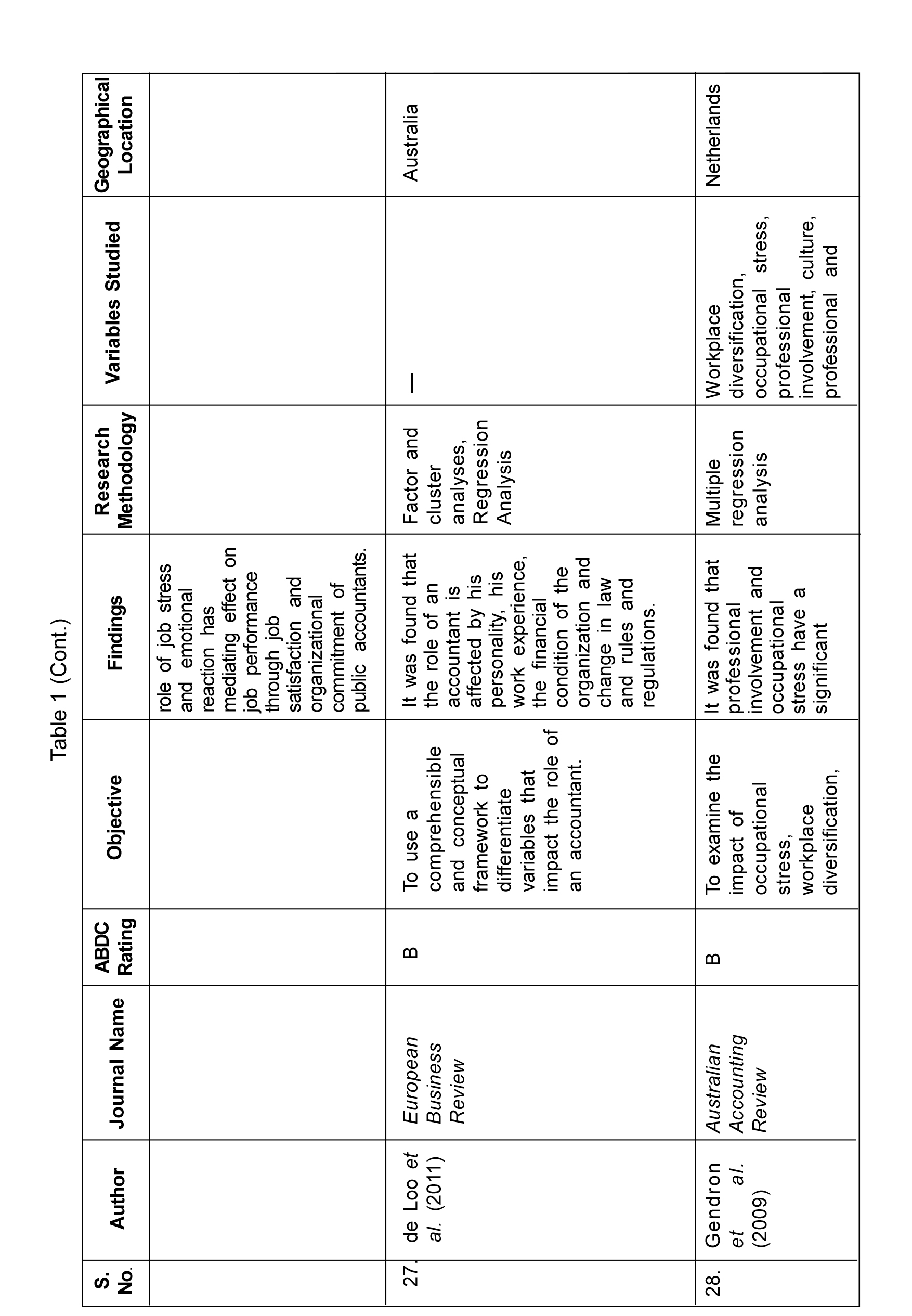

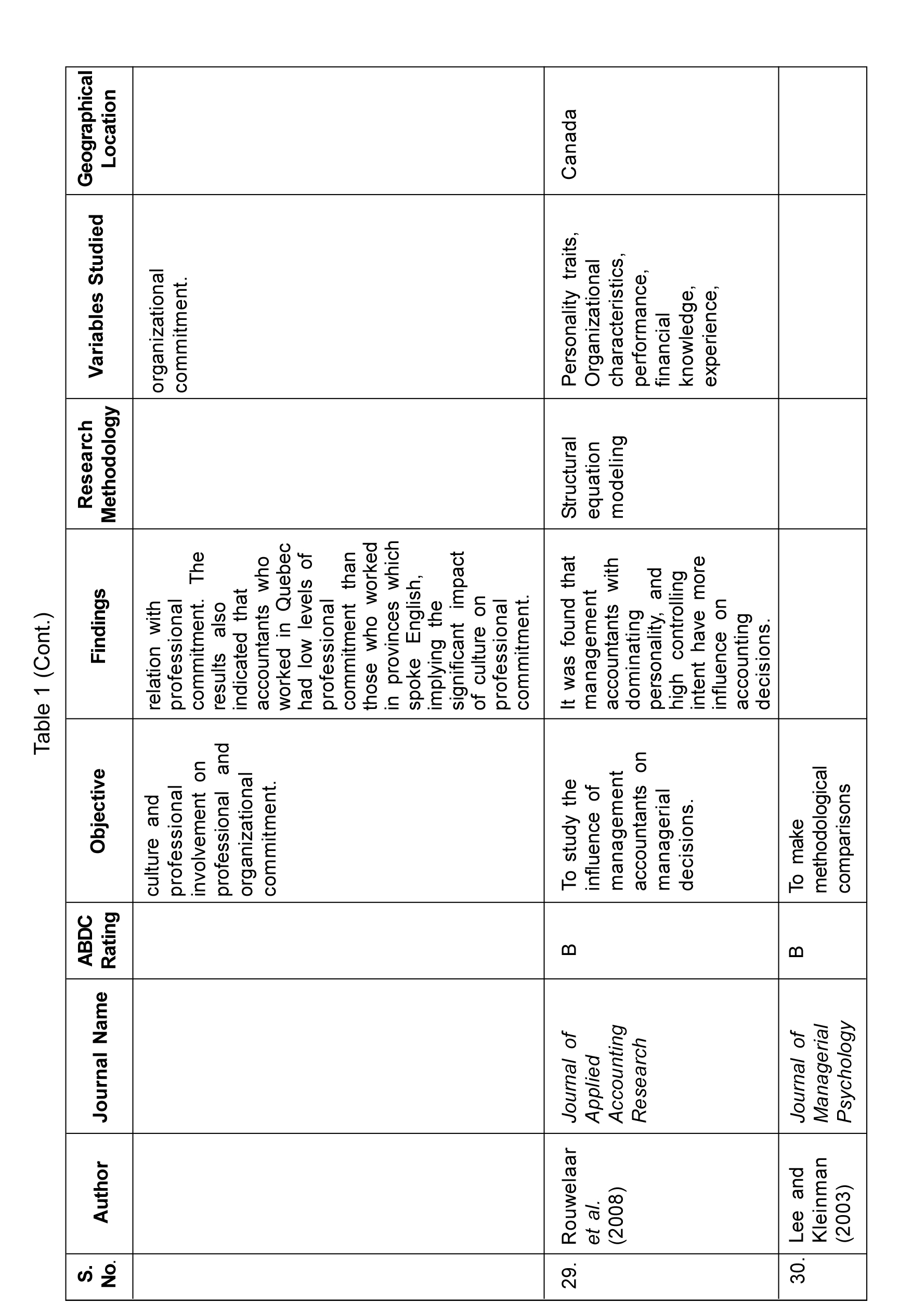

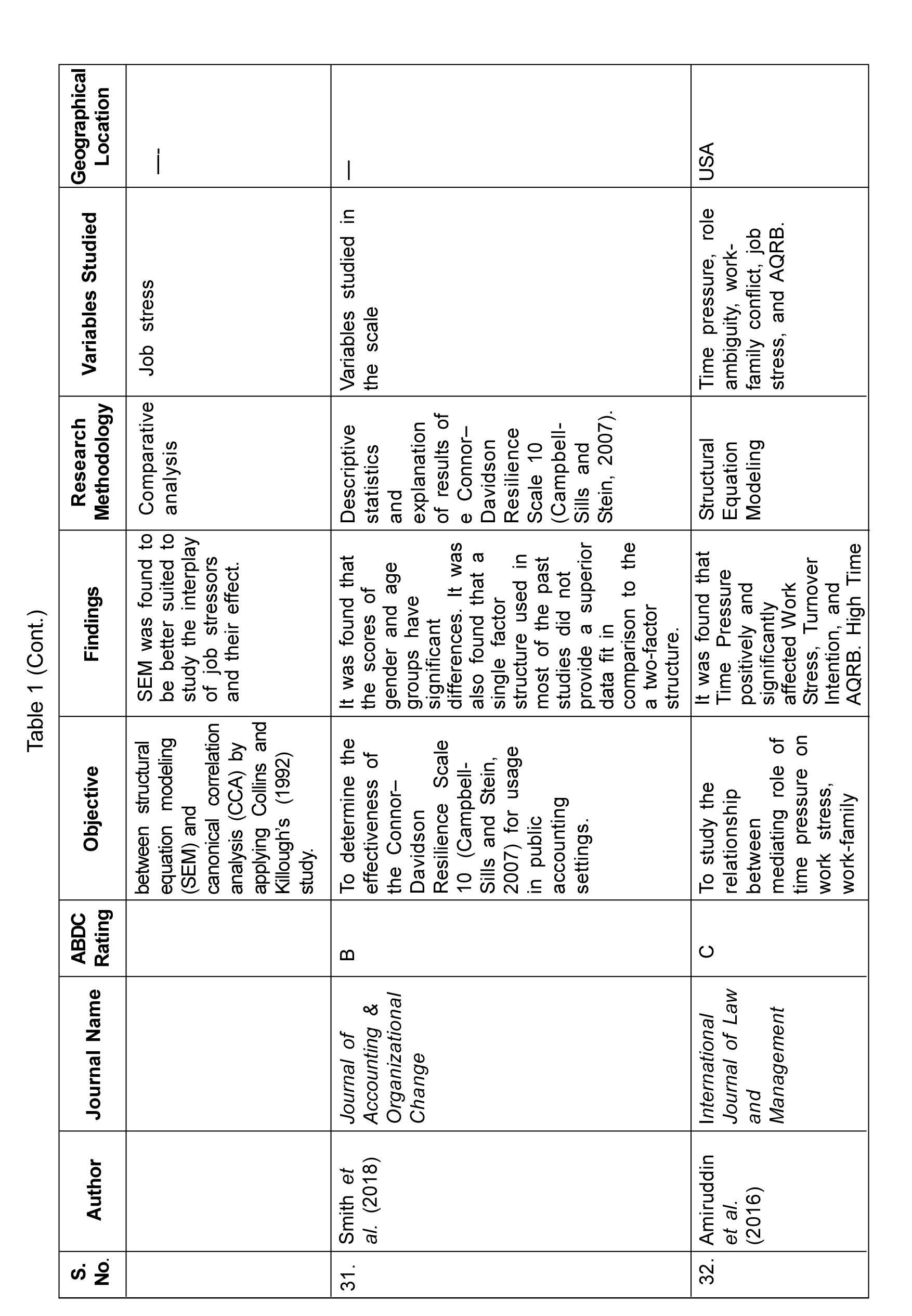

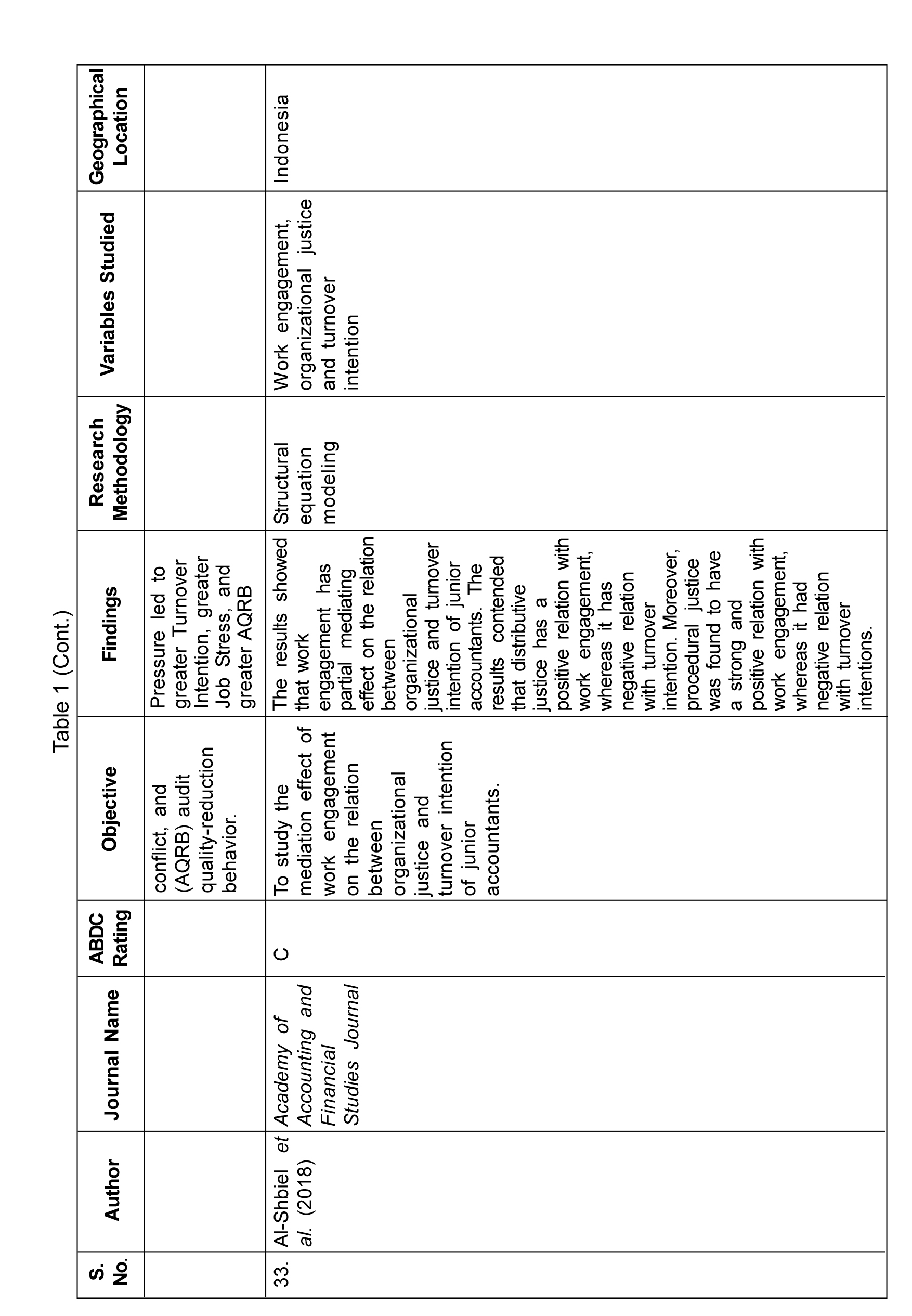

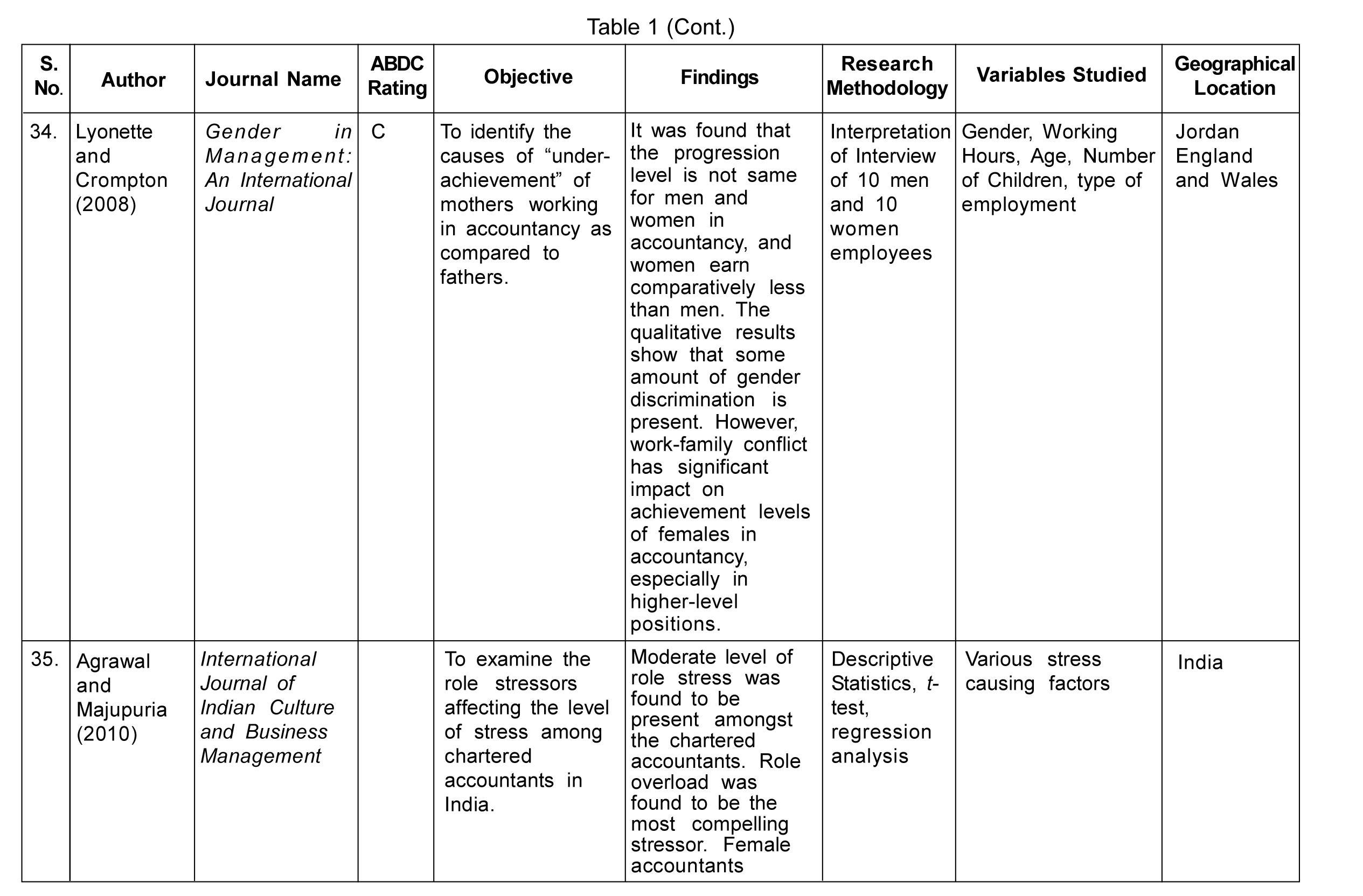

Various databases were explored with respect to occupational stress among accountants. Due to the very narrow inclusion criteria, not many research papers/articles were available which could be included in the literature review. Table 1 gives a glimpse of the studies considered for the literature review as per the ABDC list of journals.

The following points can be made about the existing literature with reference to Table 1.

Nature of Study

Most of the studies are empirical in nature and have either the antecedents of stress or their consequences or in some cases both. These studies are important to identify the variables that have been studied in the past and which can be worked upon in future. Also, various literature reviews conducted in the past have been included in the present paper.

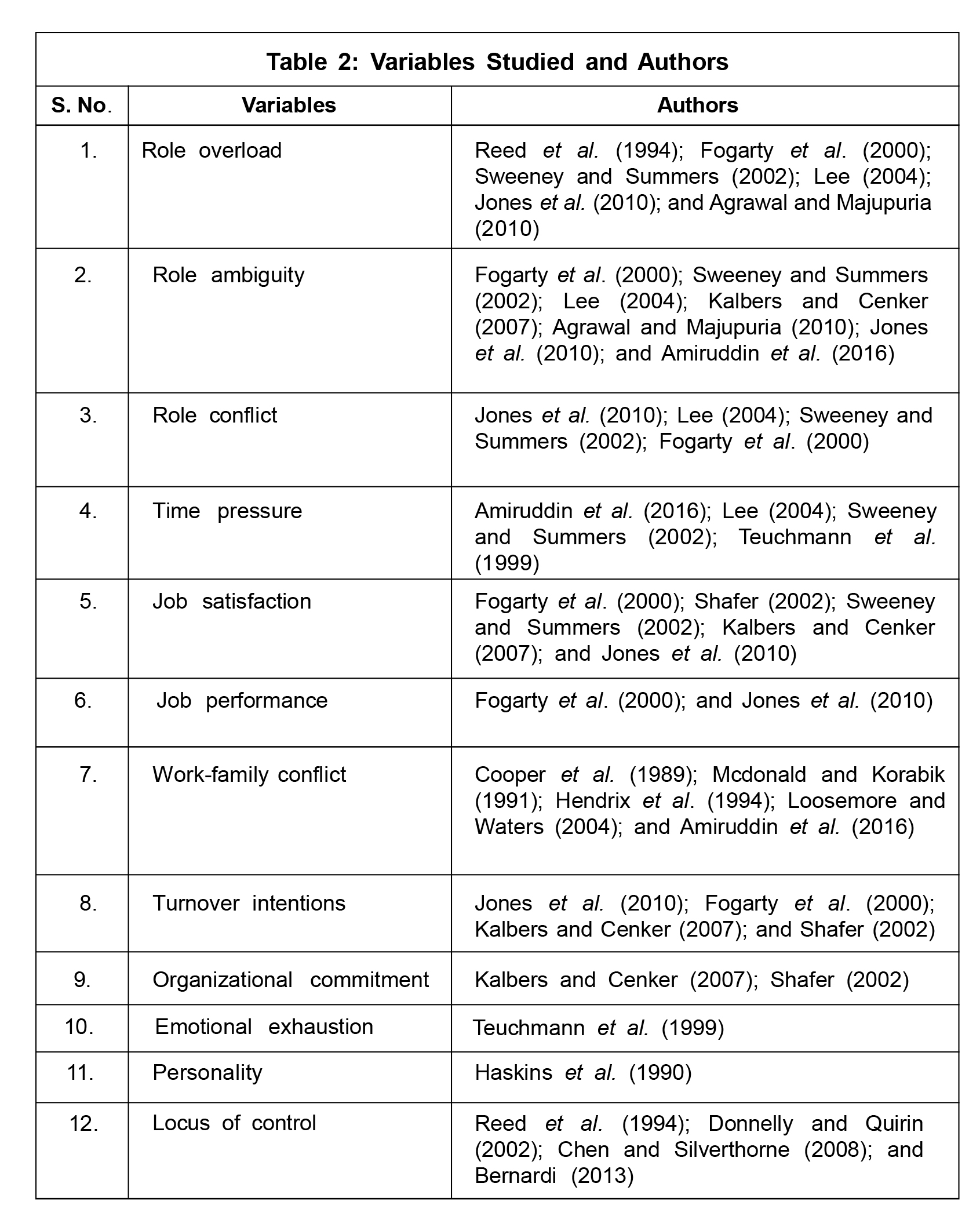

Variables Studied

Table 2 provides the variables studied and the authors associated with the study.

Major Antecedents to Occupational Stress

Based on the review of available literature, some major antecedents to occupational stress have been identified.

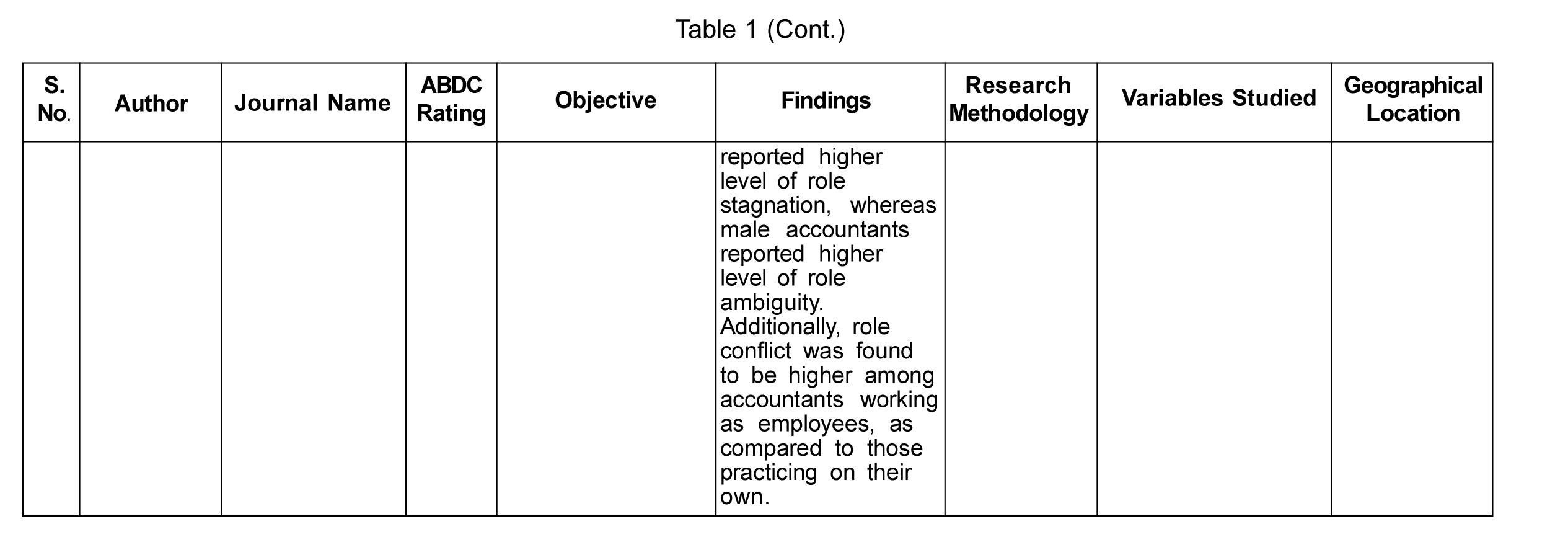

Role Stressors (i.e., Role Ambiguity, Role Conflict and Role Overload): Many researchers have concluded in their studies that there is a positive and significant relationship between role stressors and occupational stress. Role conflict is a situation in which two or more incompatible social roles overlap. Role ambiguity refers to the doubt or confusion in the mind of the individual because of incomplete information regarding his role in the organization (Hall and Savery, 1986). It has been stated that when an individual experiences higher degree of role ambiguity, role conflict and role overload, he tends to experience higher degree of occupational stress (Reed et al., 1994; Jones et al., 2010; Fogarty et al., 2000; Sweeney and Summers, 2002; Lee, 2004; Kalbers and Cenker, 2007; Agrawal and Majupuria, 2010; Amiruddin et al., 2016).

Time Pressure: Accounting professionals face a very high degree of time pressure during peak season as they have to meet tight deadlines, leaving very less time for relaxation during this time period (Sanders et al., 1995; and Fogarty et al., 2000). Accountants tend to experience a very high degree of stress during the period of busy or peak season (Teuchmann et al., 1999; Sweeney and Summers, 2002; Lee, 2004; and Amiruddin et al., 2016).

Job Satisfaction: If a person is not satisfied with his or her work then he/she is likely to have more stress (Smith, 1990). Job dissatisfaction has been seen as both the antecedent to occupational stress as well as the consequence of it. Numerous studies show a direct and positive relationship between job dissatisfaction and job stress (Fogarty et al., 2000; Sweeney and Summers, 2002; Shafer, 2002; Kalbers and Cenker, 2007; and Jones

et al., 2010)

Job Performance: Job performance is proved to have a negative relationship with occupational stress (Fogarty et al., 2000; and Jones et al., 2010). High level of job stress is associated with underperformance and low level of occupational stress has been linked with better performance at the job.

Work-Family Conflict: Women experience greater stress levels due to work-family conflict and discrimination (Cooper et al., 1989; McDonald and Korabik, 1991; Hendrix et al., 1994; and Loosemore and Waters, 2004). These findings, however, are overshadowed by results suggesting men and women experience almost similar stressors at work (Collins and Killough, 1989; and Amiruddin et al., 2016).

Turnover Intentions: Accountants with higher degree of occupational stress were found to have higher turnover intentions (Fogarty et al., 2000; Shafer, 2002; Kalbers and Cenker, 2007; and Jones et al., 2010).

Gender: Gender plays a significant role in the amount of stress experienced because of the biological differences (Piccoli et al., 1988). Social Role Theory has also been used by researchers to suggest that women have to deal with more stress than their male counterparts (Baruch et al., 1987; and Netterstrom et al., 1991). Whereas other studies claim that there is no significant difference in the level of occupational stress that both the genders experience (Rick and Guppy, 1994; Martocchino and O'Leary, 1989; and Davis et al., 1999).

Personality: Individuals who have Type-A personality tend to experience higher stress levels in comparison to people having Type-B personality because people who have Type B personality tend to remain calm and composed even in unfavorable circumstances (Kimes, 1977; Coppage and French, 1987; Piccoli et al., 1988; Haskins et al., 1990; Danna and Griffin, 1999; and Fisher, 2001). Individuals with Type A personality tend to be more hardworking and ambitious. They tend to be less patient, aggressive and determined, whereas individuals with Type B personality tend to have lower level of competitiveness, are easy-going, and do not get frustrated easily.

Locus of Control: Various studies have concluded that an individual feels less stressed when there is internal locus of control as he finds the freedom to take the decisions on his own (Bernardi, 1997; Raitano and Kleiner, 2004; Chen and Silverthorne, 2008; Hsieh and Wang, 2012; and Kumar and Jain, 2012). Lower degree of locus of control has been associated with higher degree of stress among employees (Reed et al., 1994; Donnelly and Quirin, 2002; Chen and Silverthorne, 2008; and Bernardi, 2013).

Age: Age affects the stress level experienced by an individual in both positive and negative ways. Experience gained with age, along with accumulated knowledge, enables the aged employees to cope with the existing demands better than the younger employees, whereas declining physical capacity and cognitive resources with age make it difficult for them to cope with the increasing work demands (Kirkcaldy and Furnham, 1999; and Rauschenbach et al., 2013).

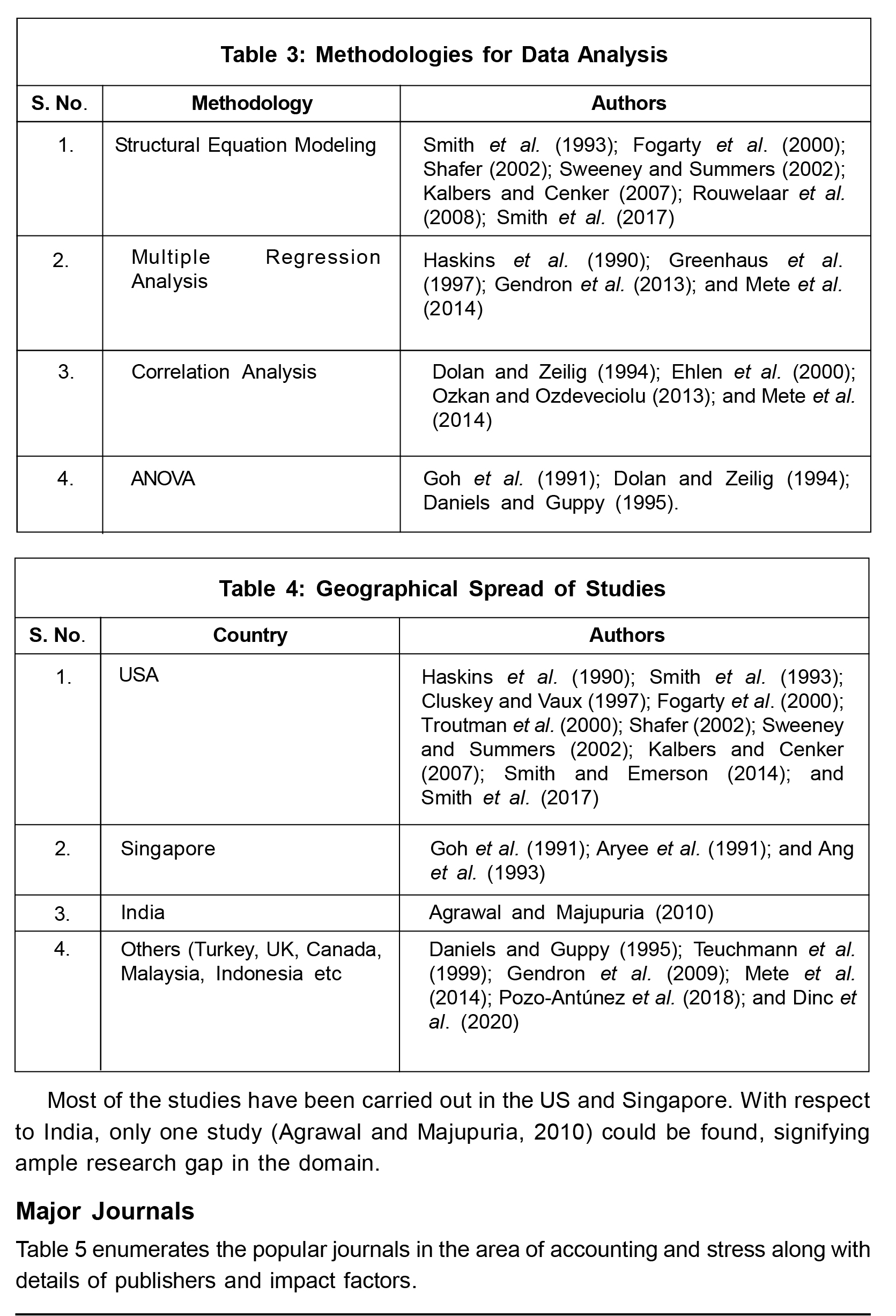

Methodology Used

In terms of the methodology used for the analysis of data in empirical research, the most commonly used research methodology has been structural equation modeling, followed by multiple regression analysis, correlation analysis and ANOVA. However, in the latest studies, structural equation modeling is found to be a more common technique to study the relationship among different variables (Table 3).

Geographical Area

Table 4 summarizes the geographical area in which the studies included in the review were conducted.

Most of the studies have been carried out in the US and Singapore. With respect to India, only one study (Agrawal and Majupuria, 2010) could be found, signifying ample research gap in the domain.

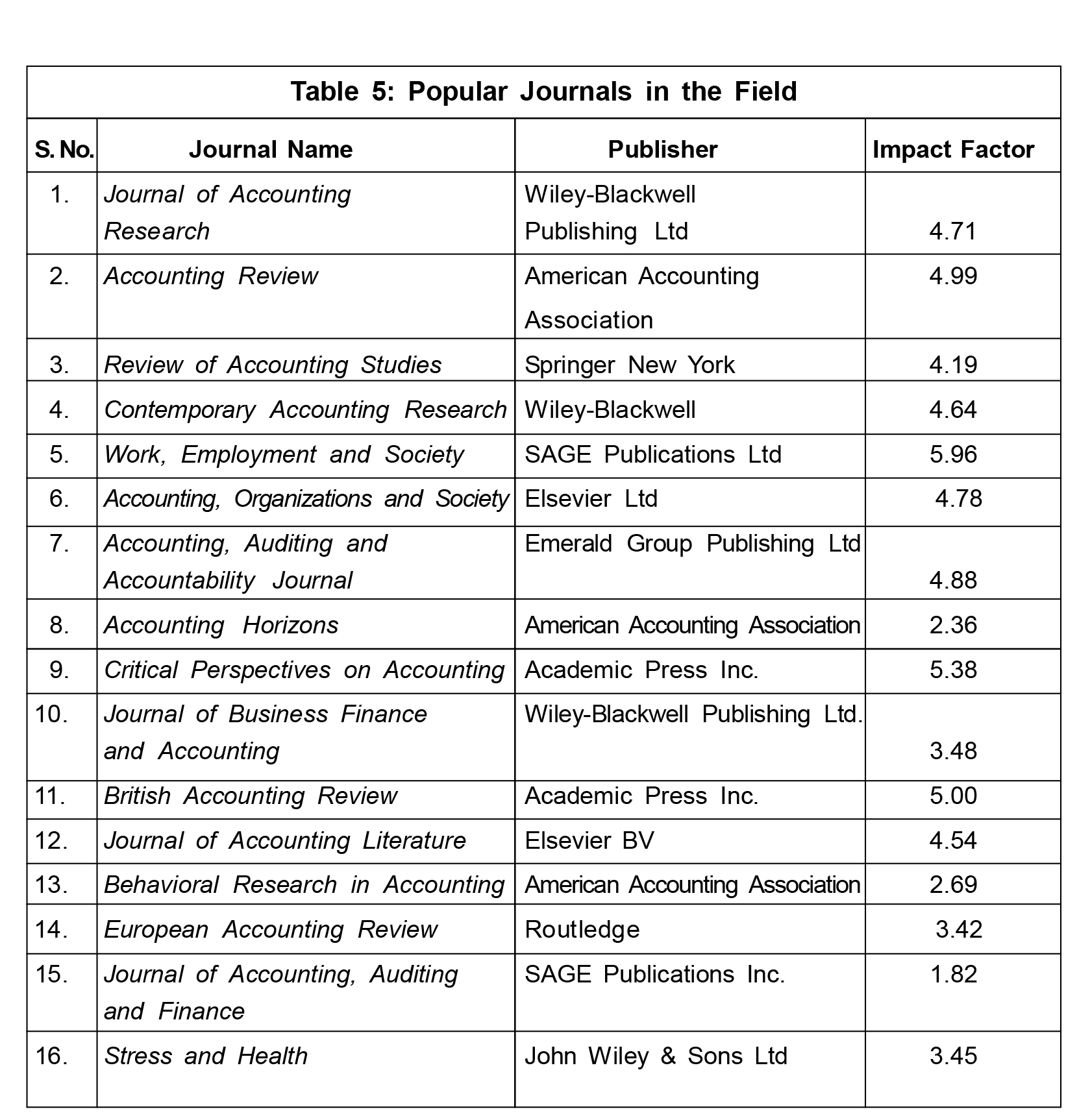

Major Journals

Table 5 enumerates the popular journals in the area of accounting and stress along with details of publishers and impact factors.

Analysis of Review

The literature review highlights the major factors which cause stress and which must be considered by the managers in order to eliminate or decrease their impact on the performance of the employee working in accounting firms. It also suggests a number of potential areas in which research can be conducted.

Various prominent as well as emerging researchers have made significant contributions to the domain of occupational stress. This study highlights the research gap in previous studies. It provides scope for future research in both theoretical and empirical ways. There is a lot of scope for identifying new factors or exploring the existing factors, which may directly or indirectly affect the level of stress among accountants.

In the light of the studies carried out earlier, some research questions concerning the research gap have been identified in the present review:

1. To study the direct effect of family income, family size, number of dependants and other variables on the level of stress among accountants.

2. To study the mediating effect of emotional intelligence, strategic thinking, affective commitment and other variables on the level of stress among accountants.

3. To study the direct effect of relationship with supervisor and peers, work culture of the organization, hierarchal structure of the organization and other variables on the level of stress among accountants.

Also, the outcomes of stress can be studied in depth with respect to mental and physical health, change in job performance, attitudinal changes and other behavioral aspects of the accountant. Here, job stress can be taken as an independent variable and the consequences of such stress can be studied. The following research questions can be worked upon:

4. To study the impact of job stress on intention to quit and job search behavior among accountants.

5. To study the impact of job stress on personal and professional relationships among accountants.

As the study shows, most of the research has been conducted in the US, which shows that the accounting firms in the US have been studied extensively. Therefore, additional research can be conducted in the nations which are still in developing phase and in which the phenomenon has not been studied extensively. Only one Indian study could be included in the literature review, which gives ample scope for future research in the area. Therefore, the following research questions can be proposed:

6. To study the difference between the stress level of accountants working in same organization (in case of an MNC) but in different nations (one country can be a developing nation and the other country can be a developed one).

7. To test the reliability and validity of prevailing scales which have been developed in advanced countries in the context of developing countries.

ANOVA, t-test, correlation, regression and Structural Equation Modeling (SEM) have been the most widely used tools of analysis in the previous studies. These tools, without any doubt, help in obtaining the most valid and reliable results.

However, other analytical techniques such as non-parametric tests which are not as common may also be applied and the validity and reliability of such analysis can also be tested.

Conclusion

Work demands and pressures may lead to workplace stress. Hence, it becomes pertinent for organizations to identify the factors that cause stress and the possible consequences of such stressors. The presence of high-level organizational stress and the negative impact of stress on workforce is a challenge for managers as well as researchers who are trying to understand job stress. A number of studies have focused on stress among accountants and its harmful effects on public accounting. Identifying the antecedents of stress and its consequences from a managerial point of view is vital to manage stress among accounting professionals. The competitive nature of the work environment and unrealistic targets are found to have a negative impact on the wellbeing of accountants.

Extensive research has been conducted on the antecedents of stress. From the review, it was found that there are not many studies in the literature that directly examine stress among accounting professionals. Time pressure, role stress, overflow of work tasks, complex work tasks, outcome uncertainty, stressed clients, client-imposed pressures and other job-related stressors are the major stress factors listed in studies.

Yet, there are still some variables which remain untouched by the researchers such as emotional exhaustion, mood, lifestyle of the employees, dynamic work environment, organizational politics, and others. These factors may have a direct or indirect impact on the level of stress among the employees. Also, the developing countries have not been studied extensively and must be given due importance in this regard. Hence, further research should be carried out to understand and minimize the negative impact of stress among accountants across the world.

Limitations and Future Scope: The limitations of the study include aspects related to time duration and population of the study. The study has not taken into consideration research conducted before 1985, and this may have led to the exclusion of some significant studies on the subject. Also, the study has taken into consideration only accounting professionals and stress related to their job. Hence, the study findings cannot be generalized.

References

- Agrawal R K and Majupuria A (2010), "An Examination of Role Stress in Chartered Accountants in India", International Journal of Indian Culture and Business Management, Vol. 3, No. 5, p. 577, https://doi.org/10.1504/ijicbm.2010.034389

- Al-Shbiel A, Al-Shbail Al-Mawali and Al-Shbail (2018), "The Mediating Role of Work Engagement in the Relationship Between Organizational Justice and Junior Accountants' Turnover Intentions", Academy of Accounting and Financial Studies Journal, Vol. 22, No. 1.

- Amiruddin, Pagalung G, Kartini and Arifuddin (2016), "The Effects of Time Pressure, Work-Family Conflict and Role Ambiguity on Work Stress and Its Effect on Audit Quality Reduction Behavior", International Journal of Law and Management, Emerald Publishing Limited, Vol. 10, No. 12, pp. 1-23.

- Ang K B, Goh C T and Koh H C (1993), "Research Notes the Impact of Age on the Job Satisfaction of Accountants", Personnel Review, Vol. 22, No. 1, pp. 31-39, https://doi.org/10.1108/00483489310025184

- Aryee S, Wyatt T and Min M K (1991), "Antecedents of Organizational Commitment and Turnover Intentions Among Professional Accountants in Different Employment Settings in Singapore", Journal of Social Psychology, Vol. 131, No. 4, pp. 545-556, https://doi.org/10.1080/00224545.1991.9713884

- Bagley P L, Dalton D and Ortegren M (2012), "The Factors that Affect Accountants' Decisions to Seek Careers with Big 4 Versus Non-big 4 Accounting Firms", Accounting Horizons, Vol. 26, No. 2, pp. 239-264, https://doi.org/10.2308/acch-50123

- Baruch G K, Biener L and Barnett R C (1987), "Women and Gender in Research on Work and Family Stress", The American Psychologist, Vol. 42, No. 2, pp.130-136. https://doi.org/10.1037//0003-066x.42.2.130

- Bernardi R A (1997), "The Relationships Among Locus of Control, Perceptions of Stress, And Performance", Journal of Applied Business Research, Vol. 13, No. 4, pp. 1-8.

- Bernard R (2013), "The Relationships Among Locus of Control, Perceptions of Stress and Performance", Journal of Applied Business Research, Vol. 13, No. 4, pp. 1-8.

- Campbell-Sills L and Stein M B (2007), "Psychometric Analysis and Refinement of the Connor-Davidson Resilience Scale (CD-RISC): Validation of a 10-Item Measure of Resilience", Journal of Traumatic Stress, Vol. 20, pp. 1019-1028, https://doi.org/10.1002/jts.20271

- Carpenter C and Hock C (2008), "The 150-hour Requirement's Effect on the CPA Exam", The CPA Journal, Vol. 78, No. 6, pp. 62-64.

- Chen J C and Silverthorne C (2008), "The Impact of Locus of Control on Job Stress, Job Performance and Job Satisfaction in Taiwan", Leadership & Organization Development Journal, Vol. 29, No. 7, pp. 572-582, https://doi.org/10.1108/01437730 810906326

- Chen J, Silverthorne C and Hung J (2006), "Organization Communication, Job Stress, Organizational Commitment and Job Performance of Accounting Professionals in Taiwan and America", Leadership & Organization Development Journal, Vol. 27, No. 4, pp. 242-249, https://doi.org/10.1108/01437730610666000

- Chong V K, Monroe G S and Soutar G N (2004), "The Impact of Emotional Reaction and Cognitive Role of Occupational Stress on Public Accountants' Performance", Asian Review of Accounting, Vol. 12, No. 1, pp. 64-78, https://doi.org/10.1108/eb0 60774

- Choo F (1986), "Job Stress, Job Performance and Auditor Personality Characteristics", Auditing: A Journal of Practice & Theory, Vol. 5, No. 2, pp. 17-34.

- Cluskey G R and Vaux A C (1997), "Is seasonal Stress a Career Choice of Professional Accountants?", Journal of Employment Counseling, Vol. 34, No. 1, pp. 7-19, https://doi.org/10.1002/j.2161-1920.1997.tb00452.x

- Cooper C L, Rout U and Faragher B (1989), "Mental Health, Job Satisfaction, and Job Stress Among General Practitioners", BMJ (Clinical Research ed.), Vol. 298, No. 6670, pp. 366-370, https://doi.org/10.1136/bmj.298.6670.366

- Collins K M and Killough L N (1989), "Managing Stress in Public Accounting", Journal of Accountancy, Vol. 167, No. 5, pp. 92-98.

- Collins K M and Killough L N (1992), "An Empirical Examination of Stress in Public Accounting", Accounting, Organizations and Society, Vol. 17, No. 6, pp. 535-547, https://doi.org/10.1016/0361-3682(92)90012-H

- Coppage R and French G R (1987), "Management of an Accounting Practice", The CPA Journal, Vol. 57, No. 6, pp. 99-101.

- Daniels K and Guppy A (1995), "Stress, Social Support and Psychological Well-Being in British Accountants", Work and Stress, Vol. 9, No. 4, pp. 432-447, https://doi.org/10.1080/02678379508256891

- Danna K and R W Griffin (1999), "Health and Well-Being in the Workplace: A Review and Synthesis of the Literature", Journal of Management, Vol. 25, No. 3, pp. 357-384.

- Davis M C, Matthews K A and Twamley E W (1999), "Is life More Difficult on Mars or Venus? A Meta-Analytic Review of Sex Differences in Major and Minor Life Events", Annals of Behavioral Medicine, Vol. 21, pp. 83-97, doi:10.1007/BF02895038.

- de Loo I, Verstegen B and Swagerman D (2011), "Understanding the Roles of Management Accountants", European Business Review, Vol. 23, No. 3, pp. 287-313, https://doi.org/10.1108/09555341111130263

- Dinc M S, Kuzey C, Gungormus A H and Atalay B (2020), "Burnout Among Accountants: The Role of Organisational Commitment Components", European Journal of International Management, Vol. 14, No. 3, pp. 443-460, https://doi.org/10.1504/EJIM.2020.107039

- Dolan S L and Zeilig P (1994), "Occupational Stress, Emotional Exhaustion and propensity to Quit Amongst Female Accountants: The Moderating Role of Mentoring", Papers 94-06, Montreal - Relations industrielles.

- Donnelly D P and Quirin J J (2002), "Occupational Stress and Turnover Issues In Public Accounting: The Mediating Effects of Locus of Control, Social Support and Employment Expectations", International Business & Economics Research Journal, Vol. 1, No. 9, pp. 75-90.

- Ehlen C R, Cluskey Jr. G R and Rivers R A (2000), "Reducing Stress from Workload Compression: Coping Strategies that Work in CPA Firms", Journal of Applied Business Research, Vol. 16, No. 3, pp. 9-13.

- Feldman D and Weitz B (1988), "Career Plateaus in the Salesforce: Understanding and Removing Blockages to Employee Growth", Journal of Personal Selling & Sales Management, Vol. 8, No. 3, pp. 23-32.

- Figler H R (1980), "Managing Stress", Management Accounting, pp. 22-28.

- Fisher R T (2001), "Role Stress, the Type A Behavior Pattern and External Auditor Job Satisfaction and Performance", Behavioral Research in Accounting, Vol. 13, No. 1, pp. 143-170.

- Fogarty T, Singh J, Rhoads G and Moore R (2000), "Antecedents and Consequences of Burnout in Accounting: Beyond the Role Stress Model", Behavioral Research in Accounting, Vol. 12, August, p. 31.

- Freudenberger H J (1980), Burnout: The High Cost of Achievement, Anchor Press, Garden City, NY.

- Friedman M, Rosenman R and Carroll V (1958), "Changes in the Serum Cholesterol and Blood Clotting Time in Men Subjected to Cyclic Variation of Occupational Stress", Circulation, Vol. 18, pp. 852-861.

- Gendron Y, Suddaby R and Qu S Q (2009), "Professional-Organisational Commitment: A Study of Canadian Professional Accountants", Australian Accounting Review, Vol. 19, No. 3, pp. 231-248, https://doi.org/10.1111/j.1835-2561.2009.00060.x

- Goh C T, Koh H C and Low C K (1991), "Gender Effects on the Job Satisfaction of Accountants in Singapore", Work and Stress, Vol. 5, No. 4, pp. 341-348, https://doi.org/10.1080/02678379108257032

- Goolsby J R (1992), "A Theory of Role Stress in Boundary Spanning Positions of Marketing Organizations", Journal of the Academy of Marketing Science, Vol. 20, No. 2, pp. 155-164.

- Greenhaus J H, Collins K M, Singh R and Parasuraman S (1997), "Work and Family Influences on Departure from Public Accounting", Journal of Vocational Behavior, Vol. 50, No. 2, pp. 249-270, https://doi.org/10.1006/jvbe.1996.1578

- Hall K and Savery L K (1986), "Tight Rein, More Stress", Harvard Business Review, Vol. 23, No.10, pp. 1162-1164.

- Haskins M E, Baglioni A J and Cooper C L (1990), "An Investigation of the Sources, Moderators and Psychological Symptoms of Stress Among Audit Seniors", Contemporary Accounting Research, Vol. 6, No. 2, pp. 361-385, https://doi.org/10.1111/j.1911-3846.1990.tb00764.x

- Hertel Guido, Thielgen Markus, Rauschenbach Cornelia et al. (2013), "Age Differences in Motivation and Stress at Work", 10.1007/978-3-642-35057-3_6.

- Hendrix W H, Spencer B A and Gibson G S (1994), "Organizational and Extra Organizational Factor Affecting Stress, Employee Wellbeing, and Absenteeism for Male and Female", Journal of Business & Psychology, Vol. 9, pp. 103-128.

- Hsieh Y and Wang M (2012), "The Moderating Role of Personality in HRM - From the Influence of Job Stress on Job Burnout Perspective", International Management Review, Vol. 8, No. 2, pp. 5-85.

- Jones A, Norman C S and Wier B (2010), "Healthy Lifestyle as a Coping Mechanism for Role Stress in Public Accounting", Behavioral Research in Accounting, Vol. 22, No. 1, pp. 21-41, https://doi.org/10.2308/bria.2010.22.1.21

- Kahn R, Wolfe P, Quinn R et al. (1964), Organizational Stress: Studies in Role Conflict and Ambiguity, John Wiley and Sons, New York.

- Kalbers L P and Cenker W J (2007), "Organizational Commitment and Auditors in Public Accounting", Managerial Auditing Journal, Vol. 22, No. 4, pp. 354-375, https://doi.org/10.1108/02686900710741928

- Kimes J D (1977), "Handling Stress in the Accounting Professions", Management Accounting, Vol. 59, No. 3, pp. 19-25.

- Kumar S and Jain A K (2012), "Essence and Consequences of Stress in the Workplace", Journal of Organisation & Human Behavior, Vol. 1, No. 3, pp. 1-11.

- Lee Larson L (2004), "Internal Auditors and Job Stress", Managerial Auditing Journal, Vol. 19, No. 9, pp. 1119-1130, https://doi.org/10.1108/02686900410562768

- Lee J (2007), "Accounting Assessment: Issues Include Qualified Workers and Industry Regulation", Orange County Business Journal, Vol. 30, pp. 30-33.

- Lee P P and Kleinman G (2003), "Statistical Choices and Apparent Work Outcomes in Auditing", Journal of Managerial Psychology, Vol. 18, Nos. 1&2, pp. 105-125, https://doi.org/10.1108/02683940310465018

- Loosemore, Martin and Waters T (2004), "Gender Differences in Occupational Stress Among Professionals in the Construction Industry", Journal of Management in Engineering, Vol. 20, No. 3, pp. 126-132.

- Lyonette C and Crompton R (2008), "The Only Way is up?: An Examination of Women's "Under-Achievement", in the Accountancy Profession in the UK, Gender in Management, Vol. 23, No. 7, pp. 506-521, https://doi.org/10.1108/17542410810908857

- Martocchio J J and O'Leary A M (1989), "Sex Differences in Occupational Stress: A Meta-Analytic Review", Journal of Applied Psychology,Vol. 7, No. 3, pp. 495-501. https://doi.org/10.1037/0021-9010.74.3.495

- McDonald L M and Korabik K (1991), "Sources of Stress and Ways of Coping Among Male and Female Managers", Journal of Social Behavior & Personality, Vol. 6, No. 7, pp. 185-198.

- Mete M, Unal O F and Bilen A (2014), "Impact of Work-Family Conflict and Burnout on Performance of Accounting Professionals", Procedia - Social and Behavioral Sciences, Vol. 131(May 2014), pp. 264-270, https://doi.org/10.1016/j.sbspro.2014. 04.115

- Netterstrom B, Kristensen T S, Damsgaard M T, Olsen O and Sjol A (1991), "Job Strain and Cardiovascular Risk Factors: A Cross Sectional Study of Employed Danish Men and Women", British Journal of Industrial Medicine, Vol. 48, No.10, pp. 684-689. https://doi.org/10.1136/oem.48.10.684

- Okeke M N, Echo O and Oboreh J C (2016), "Effects of Stress on Employee Productivity", International Journal of Accounting Research, Vol. 42, No. (3495), pp. 1-12.

- Ozkan A and Ozdeveciolu M (2013), "The Effects of Occupational Stress on Burnout and Life Satisfaction: A Study in Accountants", Quality and Quantity, Vol. 47, No. 5, 2785-2798, https://doi.org/10.1007/s11135-012-9688-1

- Piccoli J, Emig R and Hiltebeitel K M (1988), "Why is Public Accounting Stressful? Is It Especially Stressful for Woman?", The Woman CPA, Vol. 50, No. 3, pp. 8-12.

- Pozo-Antunez J J, Ariza-Montes A, Fernandez-Navarro F and Molina-Sanchez H (2018), "The Effect of a Job Demand-Control-Social Support Model on Accounting Professionals' Health Perception", International Journal of Environmental Research and Public Health, p. 15.

- Raitano R E and Kleiner B H (2004), "Stress Management: Stressors, Diagnosis, and Preventative Measures", Management Research News, Vol. 27, Nos. 4/5, pp. 32-38. https://doi.org/10.1108/01409170410784446

- Rauschenbach and Markus, Hertel, Guido and Thielgen, Cornelia and Grube, Anna and Stamov Robnagel, Christian and Krumm and Stefan (2013), "Age Differences in Motivation and Stress at Work", 10.1007/978-3-642-35057-3_6.

- Rebele J E and Michaels R E (1990), "Independent Auditors' Role Stress: Antecedent, Outcome and Moderating Variables", Behavioral Research in Accounting, Vol. 2, pp. 124-153.

- Reed S A, Kratchman S H and Strawser R H (1994), "Job Satisfaction, Organizational Commitment and Turnover Intentions of United States Accountants The Impact of Locus of Control and Gender", Accounting, Auditing & Accountability Journal, Vol. 7, No. 1, pp. 31-58, https://doi.org/10.1108/09513579410050371

- Richardson F W (2014), Enhancing Strategies to Improve Workplace Performance, Doctoral Dissertation, Walden University.

- Rick Jo and Guppy Andy (1994), "Coping Strategies and Mental Health in White Collar Public Sector Employees", European Work and Organizational Psychologist, Vol. 4, No. 2, pp.121-137, DOI: 10.1080/13594329408410479

- Rouwelaar, Bots and Loo F (2008), Journal of Applied Accounting Research. In Journal of Applied Accounting Research, Vol. 9, https://doi.org/10.1108/jaar.2008. 37509aaa.001

- Sanders J C, Fulks D L and Knoblett J K (1995), "Stress and Stress Management in Public Accounting", The CPA Journal, Vol. 65, No. 8, pp. 46-49.

- Schiltz P J and Syverud K D (1999), "On being a Happy, Healthy and Ethical Member of an Unhappy, Unhealthy and Unethical Profession", Vanderbilt Law Review, Vol. 52, No. 4 pp. 869-951.

- Shafer W E (2002), "Ethical Pressure, Organizational-Professional Conflict and Related Work Outcomes Among Management Accountants", Journal of Business Ethics, Vol. 38, No. 3, pp. 263-275, https://doi.org/10.1023/A:1015876809254

- Silvester A (2017), A Little More Conversation: Mental Health in the Changing World of Work, Institute of Directors, London.

- Smith K J (1990), Occupational Stress in Accountancy: A Review, Journal of Business and Psychology, Vol. 4, No. 4, pp. 511-524, https://doi.org/10.1007/BF01013612

- Smith K J and Emerson D J (2014), "An Assessment of the Psychometric Properties of the Perceived Stress Scale-10 (PSS10) with a US Public Accounting Sample", Advances in Accounting, Vol. 30, No. 2, pp. 309-314, https://doi.org/10.1016/j.adiac.2014.09.005

- Smith K J, Derrick P L and Koval M R (2010), "Stress and its Antecedents and Consequences in Accounting Settings: An Empirically Derived Theoretical Model", In Advances in Accounting Behavioral Research, Vol. 13, https://doi.org/10.1108/S1475-1488(2010)0000013009

- Smith K J, Emerson D J and Everly G S (2017), "Stress Arousal and Burnout as Mediators of Role Stress in Public Accounting", Advances in Accounting Behavioral Research, Vol. 20, pp. 79-116, https://doi.org/10.1108/S1475-148820170000020004

- Smith K J, Emerson D J and Schuldt M A (2018), "A Demographic and Psychometric Assessment of the Connor-Davidson Resilience Scale 10 (CD-RISC 10) with a US Public Accounting Sample", Journal of Accounting and Organizational Change, Vol. 14, No. 4, pp. 513-534, https://doi.org/10.1108/JAOC-12-2016-0085

- Smith K J, Everly G S and Johns T R (1993), "The Role of Stress Arousal in the Dynamics of the Stressor to Illness Process among Accountants", Contemporary Accounting Research, Vol. 9, No. 2, pp. 432-449, https://doi.org/10.1111/j.1911-3846.1993.tb00890.x

- Sorensen J and Sorensen T (1974), "The Conflict of Professionals in Bureaucratic Organizations", Administrative Science Quarterly, Vol. 19, pp. 98-106.

- Spillane R (1987), "How Auditors Can Manage Stress and Motivation", Managerial Auditing Journal, Vol. 2, No. 2, pp. 26-28, https://doi.org/10.1108/eb017594

- Stevenson D and Farmer P (2017), "Thriving at Work: The Independent Review of Mental Health and Employers". Retrieved from https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/658145/thriving-at-work-stevenson-farmer-review.pdf. Accessed on January 6, 2021.

- Sweeney J T and Summers S L (2002), "The Effect of the Busy Season Workload on Public Accountants' Job Burnout", Behavioral Research in Accounting, Vol. 14, No. 1, pp. 223-245, https://doi.org/10.2308/bria.2002.14.1.223

- Teuchmann K, Totterdell P and Parker S K (1999), "Rushed, Unhappy and Drained: An Experience Sampling Study of Relations Between Time Pressure, Perceived Control, Mood and Emotional Exhaustion in a Group of Accountants", Journal of Occupational Health Psychology, Vol. 4, No. 1, pp. 37-54, https://doi.org/10.1037//1076-8998.4.1.37

- Troutman C S, Burke K G and Beeler J D (2000), "The Effects of Self-Efficacy, Assertiveness, Stress and Gender on Intention to Turnover in Public Accounting", Journal of Applied Business Research. Vol. 16, No. 3, pp. 63-74.

- Viator R E (2001), "The Association of Formal and Informal Public Accounting Mentoring with Role Stress and Related Job Outcomes", Accounting, Organizations and Society, Vol. 26, No. 1, pp. 73-93.

- Williams E S, Konrad T R, Scheckler W E et al. (2001), "Understanding Physicians' Intentions to Withdraw from Practice: The Role of Job Satisfaction, Job Stress, Mental and Physical Health", Health Care Management Review, Vol. 26, No. 1, pp. 7-19.

- Wood D J and Wilson J A (1988), "Stress and Coping Strategies in Internal Auditing", Managerial Auditing Journal, Vol. 3, No. 2, pp. 8-16, https://doi.org/10.1108/eb002805